.png)

REUTERS/Dinuka Liyanawatte

- Americans are already feeling the pain of higher bond yields.

- Bond yields have surged in recent weeks as investors fret over higher-for-longer interest rates.

- Borrowing costs have climbed for mortgages, personal loans, auto loans, and credit card debt.

Higher interest rates are signaling more pain ahead for American consumers, and there are signs that the impact of the recent surge in US Treasury yields is already starting to be felt.

Treasury yields have jumped over the past month as investors fret over higher-for-longer interest rates from the Fed. That pushed the 10-year Treasury yield past 5% on Monday, the highest level since 2007.

Rising bond yields spell trouble for consumers in particular, since they influence higher borrowing costs across the economy.

There are signs that could already be starting to weigh on Americans, who look to be in a more precarious financial position as their savings dwindle.

Here are four charts that show Americans are already feeling the pain from surging bond yields:

1. Mortgage rates topped 8%.

Mortgage News Daily

The 30-year fixed mortgage rate just climbed above 8%, according to an estimate from Mortgage News Daily. That reflects the highest cost of borrowing in 23 years for one of the most popular American mortgages.

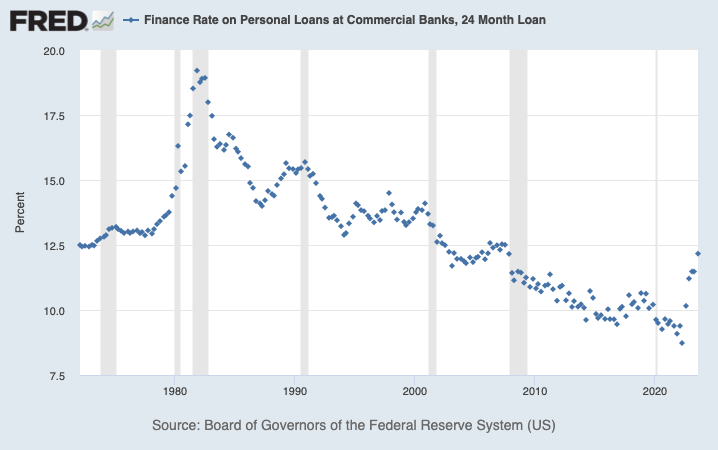

2. Personal loan rates are rising.

Federal Reserve

The 24-month personal loan rate at commercial banks hit 12.17%, according to Federal Reserve data. That's the highest cost of borrowing for personal loans since 2007.

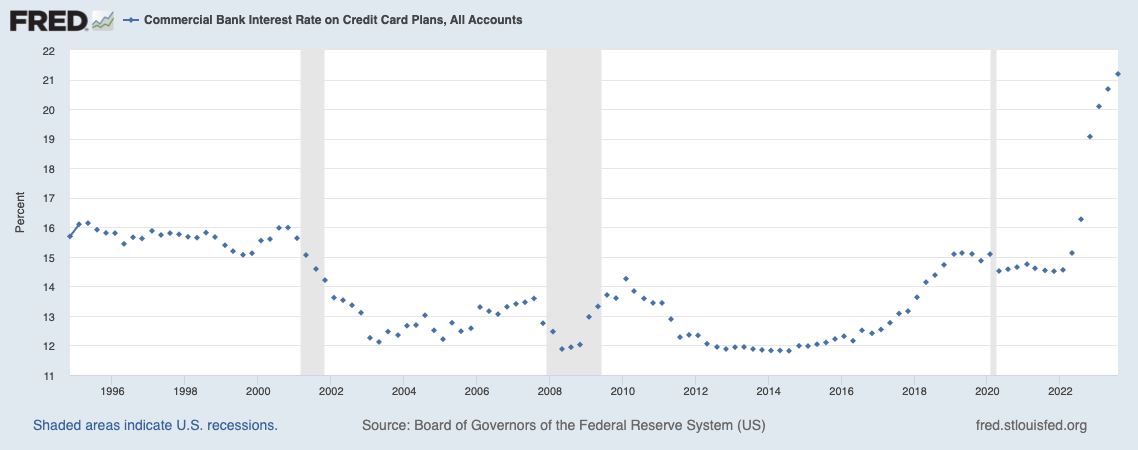

3. Interest rates on credit card debt are rising.

Federal Reserve

Commercial bank interest rates on credit cards soared to 21.19% in August of this year, Fed data shows. A separate analysis from Bankrate pegged the average retail card interest rate around 28.93%, the highest on record.

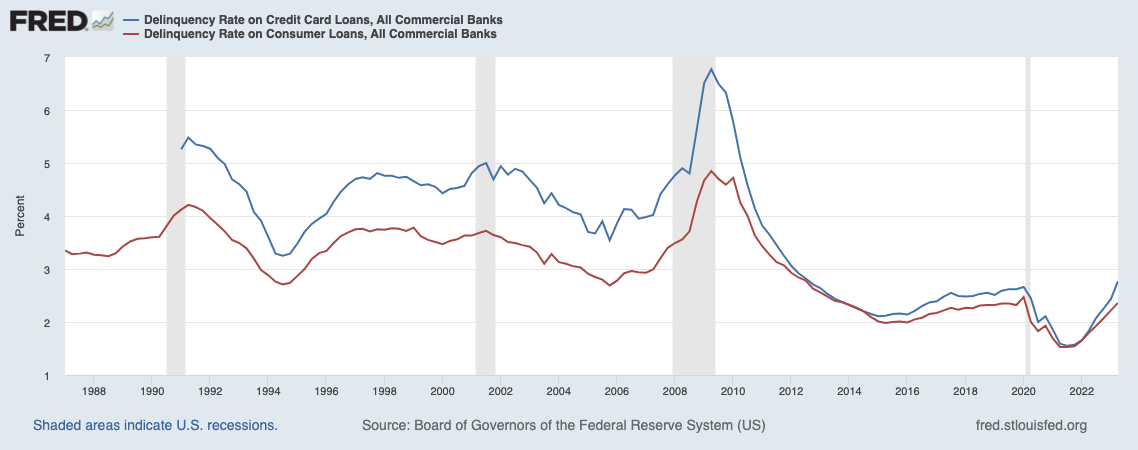

4. Delinquencies are rising - and could rise further.

Federal Reserve

Late payments are piling up for consumers who are struggling to meet rising interest costs on their debts. Credit card delinquencies in the the second quarter were at the highest rate since 2012. Meanwhile, consumer loan delinquencies hit their highest level since the pandemic.

And that trend could get worse, considering the ballooning balance of non-mortgage consumer debt, which typically isn't financed at a fixed rate.

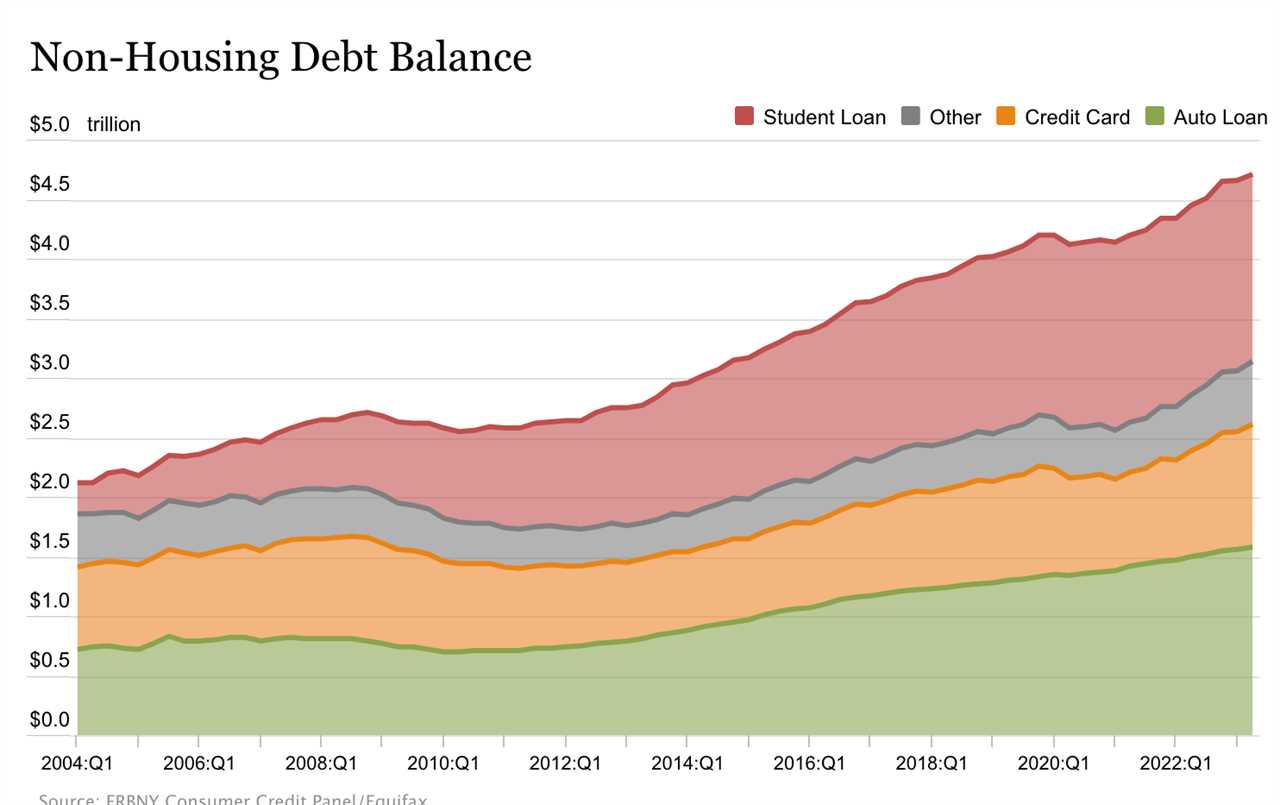

Non-mortgage debt rose to $4.71 trillion in the second quarter, according to New York Fed data. A record $1.03 trillion is comprised of credit card debt, while $1.58 trillion is made up of auto loans.

Meanwhile, there's around $1.57 trillion of student loan debt. Payments for borrowers just resumed as of the start of October, though 34% of borrowers said they won't be able to make payments at all, according to a recent Morgan Stanley survey.

Federal Reserve Bank of New York

Read the original article on Business Insider

------------Read More

By: [email protected] (Jennifer Sor)

Title: The impact of soaring bond yields on US consumers in 4 charts

Sourced From: markets.businessinsider.com/news/bonds/us-treasury-crash-bond-yields-debt-interest-rates-consumer-spending-2023-10

Published Date: Mon, 23 Oct 2023 16:34:58 +0000