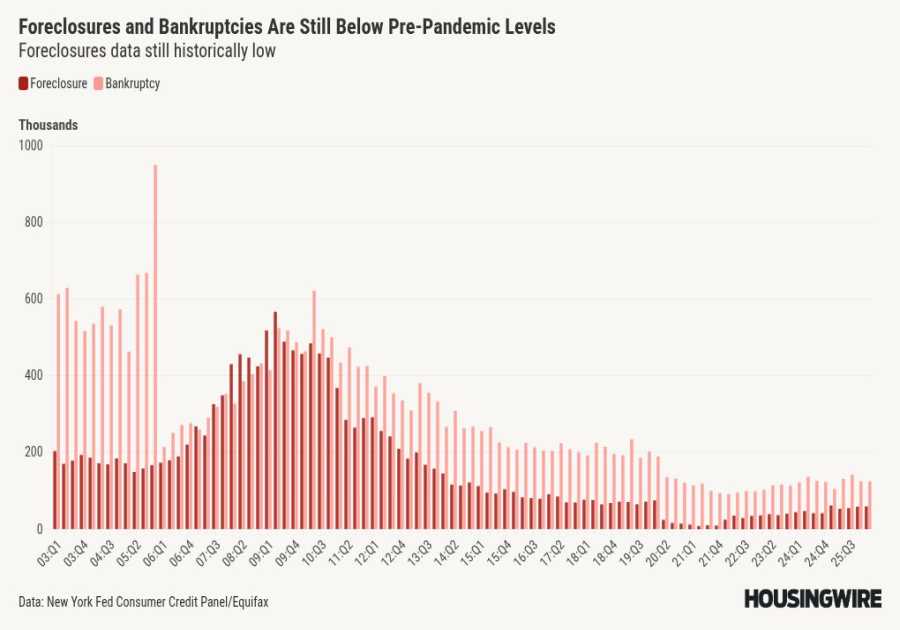

.png)

For the past several years, the housing market has been defined more by what didn’t happen than what did.

Homeowners didn’t move. Inventory didn’t rebuild. Affordability didn’t materially improve. Ultra-low pandemic-era mortgage rates created a lock-in dynamic unlike any in modern housing history, freezing mobility and pushing existing-home sales toward decade lows.

As 2026 approaches, the housing market is not on the cusp of a dramatic turning point. Instead, several trends visible in 2025 appear likely to continue shaping conditions. The coming year is more likely to extend a slow thaw than deliver a breakout.

Three forces, in particular, will matter most: uneven affordability improvement, life event-driven housing demand, and a gradual rise in inventory as the grip of the rate lock-in effect loosens at the margins.

Affordability: Improving at the edges but uneven across the map

According to the First American Real House Price Index, which adjusts prices for income and interest rate changes, housing affordability has posted its longest stretch of annual improvement since late 2019 and early 2020.

Wage gains outpaced home-price appreciation in 2025 and mortgage rates eased off their peaks, helping repair some of the damage. But the progress has been far from uniform.

Nationally, house-price appreciation has cooled to its slowest pace since 2012, according to First American Data & Analytics. In markets where inventory has expanded — often in the South and West, where construction pipelines remain active and sellers have reset expectations — buyers are regaining leverage, and affordability may continue to improve in 2026 as incomes and prices realign.

But that does not apply everywhere. Many markets in the Northeast and Midwest remain supply constrained, keeping price pressures elevated. Limited inventory and persistent competition leave little room for meaningful affordability relief.

Affordability in 2026 is likely to remain a patchwork — improving where supply is loosening and remaining stubborn where the market has yet to recalibrate.

Life happens: Demographics and milestones quietly reawaken demand

If affordability determines the feasibility of buying a home, life events determine the necessity. After several years in which many households delayed major housing decisions, life’s usual drivers — marriage, separation, new children, aging parents, job relocations and downsizing — are beginning to exert more influence again.

From 2022 through 2025, existing-home sales fell roughly 4 million transactions short of the pre-pandemic norm. These “missing” moves represent pent-up demand from households that, under typical conditions, would have transitioned into different homes. The longer these moves are postponed, the more pressure builds beneath the surface.

Turn data into decisions at the Housing Economic Summit

Join top economists and industry leaders Feb. 10 in Dallas

Secure your seatDemographics intensify this momentum. Nearly 52 million Americans are now in their 30s, a decade that has historically coincided with first-time homeownership as well as growing families and major life transitions.

According to a First American analysis, millennials are expected to add more than 10 million homeowner households over the next 25 years. Even with mortgage rates in the low-6% range, many households will reach stages of life where staying put is no longer practical.

In 2026, life event-driven demand may not generate a surge, but it can create a steady, organic lift in market activity. The cumulative weight of everyday life decisions — rather than a single macroeconomic trigger — could become a key force to nudge sales higher.

Inventory: Gradual thaw as lock-in effect slowly loosens its grip

After years of scarcity, inventory began to turn a corner in 2025. By the inventory turnover measure — total homes for sale as a share of total households — supply increased from roughly 14 homes for sale in every 1,000 to nearly 15 homes for sale.

This remains well below the historic average of closer to 25 homes for sale in every 1,000, yet the direction is meaningful.

Next year may extend this gradual upward trend. More households recognize that mortgage rates may remain higher for longer, prompting moves driven by need rather than rate optimization. And as life events encourage mobility, more existing homeowners may list their homes despite holding mortgages well below prevailing rates.

As with affordability, regional patterns will differ sharply. Some markets already show inventory levels above their 2018-2019 averages, while others remain structurally undersupplied. The speed at which inventory rebuilds will influence everything from price trends to time on market, shaping local conditions far more than national averages.

Market defined by movement, not a breakout

If 2025 marked the beginning of a slow thaw, 2026 may continue that trajectory. Affordability will make incremental, uneven gains. Life events and demographics will quietly push more households into buying and selling decisions. Inventory will edge higher as the lock-in effect loosens — not dramatically, but consistently enough to matter.

The year ahead is unlikely to deliver a swift return to “normal,” yet it may bring something just as important — progress, along with a market shaped less by headline mortgage rates and more by the people and places that ultimately drive housing demand and supply.

Don’t settle for only the data. Learn how to harness it to make better and faster decisions. Find the signal at the Housing Economic Summit. Join us in Dallas on Feb. 10.

Read More

By: Odeta Kushi

Title: 3 forces shaping the housing market in 2026

Sourced From: www.housingwire.com/articles/housing-market-2026-trends/

Published Date: Fri, 12 Dec 2025 17:24:40 +0000