.png)

Economic reports over the Thanksgiving holiday paint a complicated picture of what’s happening, and where we are on recession watch. The big economic surprise was the strength of Black Friday sales, where consumers spent a record $9.12 billion online. Another surprise was the Atlanta Fed’s forecast of 4.3% GDP growth in the fourth quarter, since the Atlanta Fed data was used by many to say that the U.S. went into a recession earlier in the year.

The jobs data, however wasn’t a surprise: the unemployment rate is now 3.7% and jobless claims are still very low historically.

With all the data we now have in front of us, we can say that the U.S. did not go into a recession at the start of 2022. The question now is whether there is a way to avoid the job-loss recession we’re facing in 2023.

The U.S. housing market went into recession in June of this year, which I talked about a few months ago on CNBC. A recession means that sales and production are down. New and existing home sales are falling, along with housing permits and starts, as we have too many new homes for the builders to issue new permits.

The job loss recession is already here in the housing market, and total incomes are falling with less volume in this sector. Although we don’t have this in the larger economy yet, housing traditionally gets weaker into a recession as it is a rate-sensitive sector of our economy.

The Federal Reserve has forecast a 4.4% unemployment rate next year, which would mean an immediate 1% increase from the cycle lows in the unemployment rate, which again implies the job loss recession is something they’re looking for (I would even say want).

Why do they want a job loss recession? Their main goal is to bring down inflation, and Americans losing their jobs is the fastest way to create more labor supply and weaker demand. Accordingly, I raised my sixth (and last) recession red flag on Aug. 5.

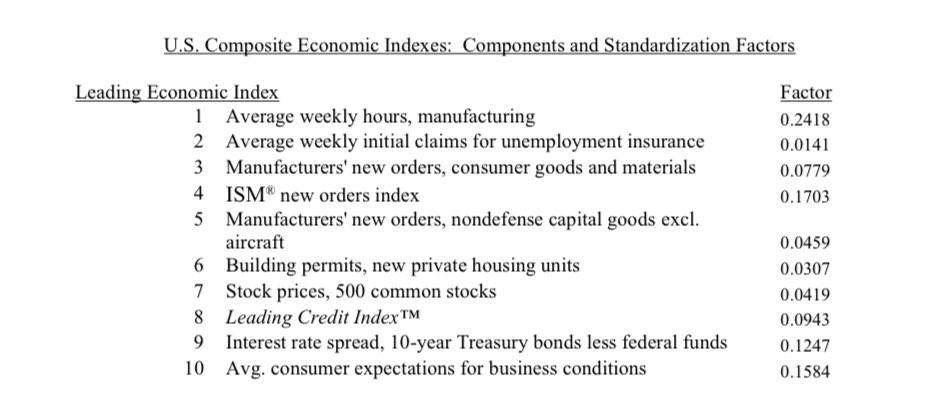

It was apparent on Aug. 5 that the leading economic index was in a downtrend that is similar to every single recession we have seen for decades. The most recent leading economic index report has confirmed that the downtrend in the data is still intact.

I discussed this with the Conference Board earlier this year as I presented my six recession red flag model to them. As always, with any index, you need to know the components and their weighting and understand how those components will look in the future.

“The US LEI fell for an eighth consecutive month, suggesting the economy is possibly in a recession,” said Ataman Ozyildirim, senior director of economics, at The Conference Board in November. “The downturn in the LEI reflects consumers’ worsening outlook amid high inflation and rising interest rates, as well as declining prospects for housing construction and manufacturing.

So with all these factors in place — housing already in a recession, the Fed’s recent actions and dealing with inflation — can we avoid this job loss recession? Yes, we can. It will be hard, and we will need a lot of help, but there is a pathway to this.

Two things need to happen

1. Inflation growth rate and long bond yields need to go down together.

The Fed is bent on driving us into a recession to make it easier to achieve their single mandate to bring down inflation. We have already seen some of the growth rates of inflation falling.

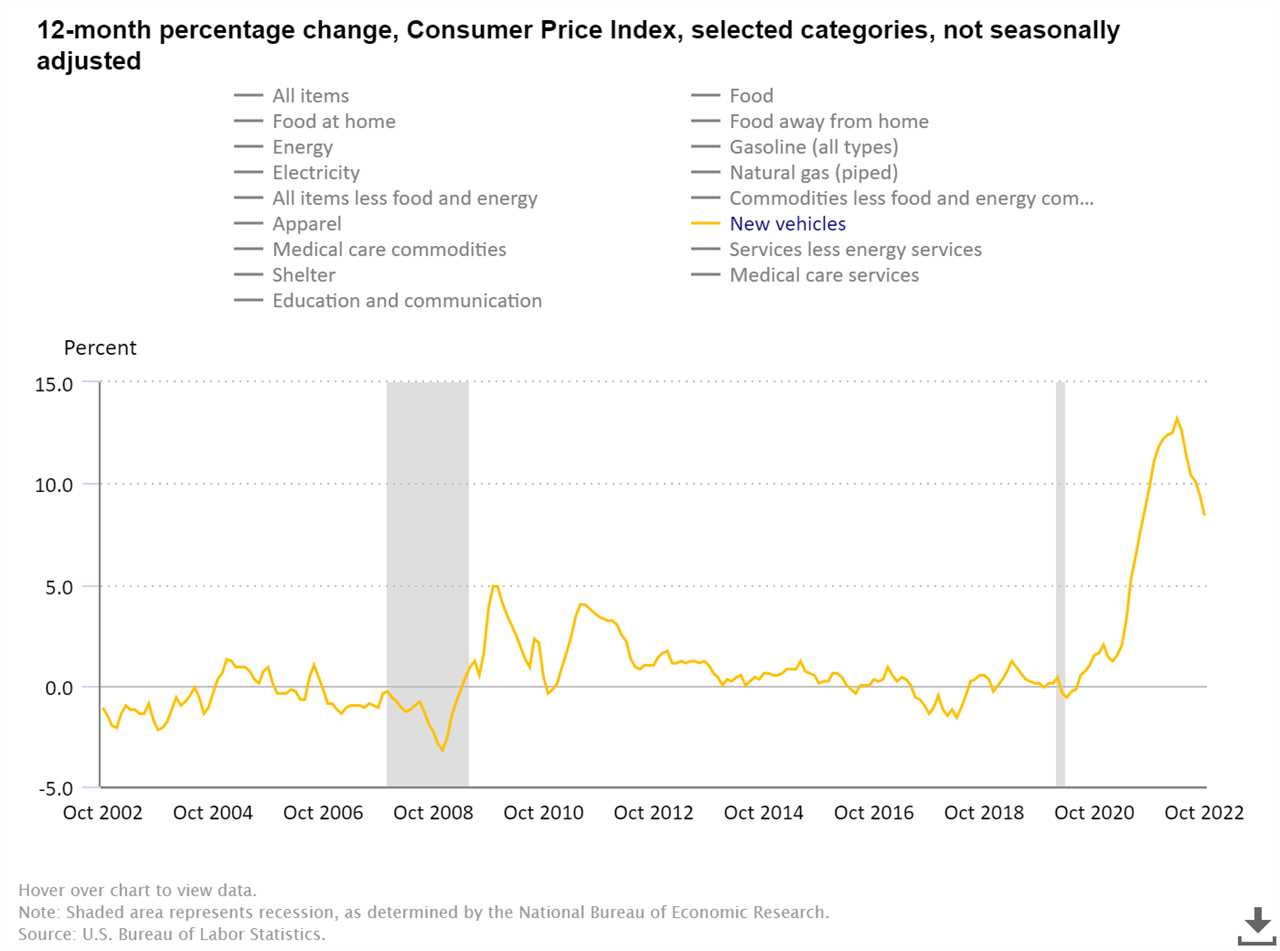

The used and new car price growth rate is falling. As you all know, car production was terrible during the global pandemic, and we are working our way back to some sense of normal in auto production.

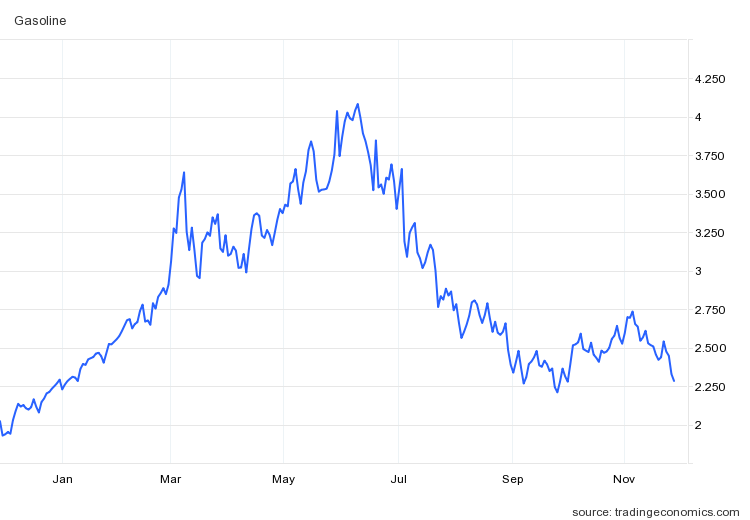

Gasoline prices are also falling. We have a lot of variables here that are out of our control that make this sector a bit abnormal today, including the Russia wild card, releasing a lot of strategic reserves, and OPEC’s view of us. However, for now, gas prices are down.

In addition, prices paid for transportation of products from China to the U.S. are falling from the COVID-19 peaks. China’s economy is in terrible shape with constant lockdowns. However, with less demand for goods from China, we are receiving less stuff and our port backlogs are resolving as we have become a bit more efficient at the ports.

We used to have tons of boats in the waters of the Pacific waiting to be docked to take stuff to the stores. Now, this stressful aspect of transportation costs is gone and the fear of a downturn in the freight industry is taking hold.

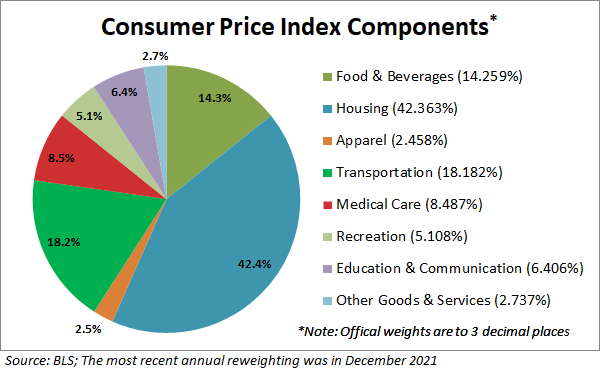

However, the biggest component of inflation isn’t the transportation cost of goods from China to the U.S., it’s rent shelter inflation, which makes up 42.2% of the consumer price index.

Housing is the significant X factor in our economy; I believe the growth rate of shelter inflation is already cooling off, it just won’t get picked up on the CPI date until next year.

In September, when the CPI inflation data was being reported on, I talked with CNBC about how this data line lags with the CPI data. In addition, we have a lot of two-unit construction built, which will bring more supply online.

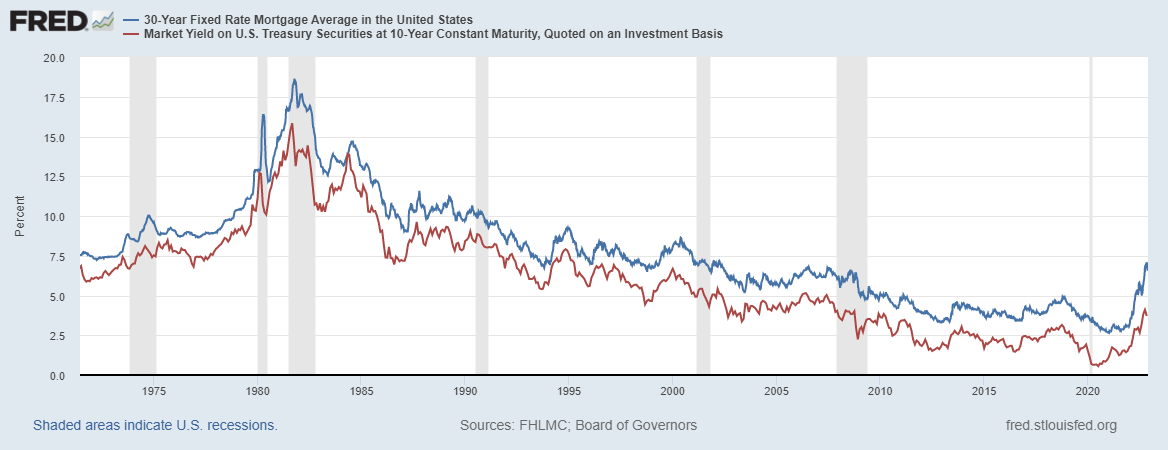

If we can get this to happen, the Fed can end their rate hikes once they get to their desired level over the next few months. If the bond market’s long end can fall, we can get mortgage rates back down to 5%.

Why does 5% matter?

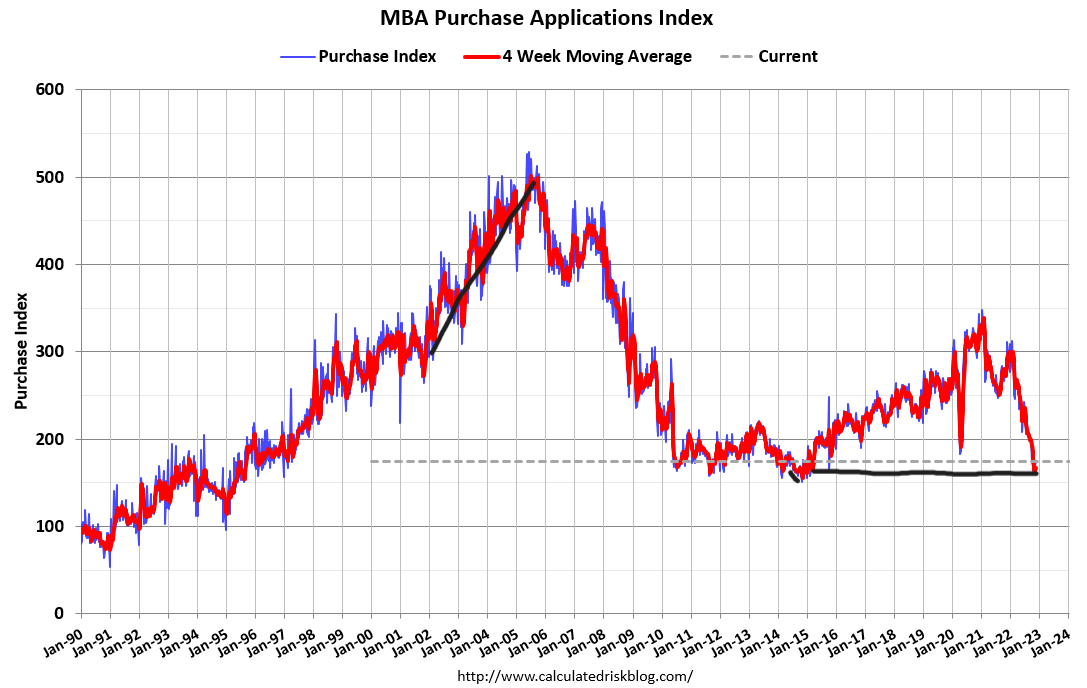

Currently, rates have fallen from 7.375% to 6.62%, which has boosted the weekly demand data to be positive for three weeks. Last week we had a decline in the year-over-year negative data, which went from 46% year-over-year declines to 41%.

Remember, a big talking point of mine is that we would have hard comps starting in October of this year on a year-over-year basis. Last year, purchase application data volume was rising late in the year, which was abnormal. I have talked about having 35% to 45% year-over-year declines as the norm from October to January, with a possible 53% to 57% decline if demand gets worse. Well, since October, the year-over-year declines have been between 39%-46%.

If mortgage rates keep going lower and we get more weekly data growth, we do need to see a noticeable year-over-year decline to warrant talk of stabilization. Right now we are working from a shallow bar, so we need to show context with the recent moves in purchase application data.

The housing market getting some stabilization will be a plus as we saw some buyers come into the marketplace with rates at 5%. Rates also need to stay at that lower for longer as well. What can’t happen is mortgage rates above 7%, since that level hasn’t fueled new listings, which means less demand, and the builders simply are done building anything new with rates that high.

However, getting mortgage rates lower with duration will help housing. The one issue here is that total inventory levels in America are still historically low, and the Fed does not want home prices to explode higher. This might prevent them from aiding housing in any meaningful way because of the fear of what we saw in 2020 and 2021; it was savagely unhealthy.

NAR total inventory data: 1,220,000 listings

The key here is that if the growth rate of inflation falls and mortgage rates can get back toward 5% with some duration, that can stop the bleeding in the one sector of the economy that is in a recession. Also, lower mortgage rates means those households that bought homes with higher rates recently can refinance if they can qualify.

2. The Fed pivots early when the labor market starts to get bad

Fed Chairman Powell will have a speaking engagement this Wednesday, so we might have the Grinch for Christmas speech about how Americans need to feel more pain for his jolly Fed members to get their job done taking down inflation. Aside from that, I don’t believe the Fed pivots until the jobs market starts to break.

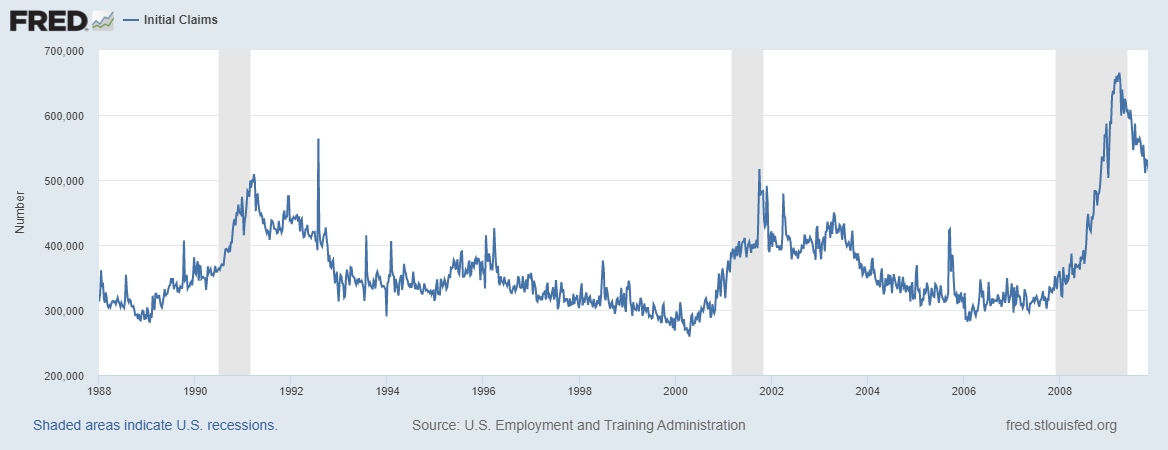

My target for the Fed pivot is that jobless claims break above 323,000 on the four-week moving average. The last headline print came in at 240,000, so we aren’t close to breaking over that number yet on a four-week moving average.

This level isn’t a high level historically when we look at jobless claims data. However, considering how low we got in jobless claims at 166,000 and where the job openings data is currently, if we break above 323,000, the Federal Reserve will get its beloved job loss recession because once jobless claims break, the downturn has just started.

The chart below shows initial jobless claims and the shaded grey parts define when we are in a recession. The chart shows the last three recessions, not including the COVID-19 recession. As you can see below, when jobless claims have an aggressive rise working from a low level, the job loss recession is happening.

If the Fed can pivot and show that they’re once again a dual mandate Fed, which means they care about employment, then the damage is done early on and can be acted on quickly by the Fed.

This is where it gets tricky since the Fed has talked about not cutting rates when the economy gets weaker and has harped on Americans feeling more pain for their job to be done. For now, the strong balance sheets of American households have kept consumption going. But, as short-term rates rise, Americans will feel it on their credit cards, home equity lines, and any mortgage rates that have recast.

The Fed believes the strength of the U.S. consumer gives it some cover to hike rates aggressively. To this point, I agree with the Fed; the consumer balance sheets look good, but you shouldn’t rely on your top horse to win every time.

We hear a lot of talk about recession. In addition, we know housing is in a downturn, manufacturing data is looking weaker, the global economies are struggling, China is a giant mess, Europe is dealing with an economic war with Russia and even my six recession red flags are raised. History has shown us time and time again that a recession isn’t that far away when a lot of these data lines turn negative together, all with the Fed raising rates.

However, what we have here in America is different than other countries; we are the only economic superpower in the world. We have solid household balance sheets and a massive young workforce that can replace older workers and consume goods and services.

We fixed some of the economic sins of the past and had the longest economic and job expansion in history before COVID-19 created a brief recession. We recovered from that recession quickly when so many people said we would be in a depression after that event. Some of those factors that convinced me that we would recover in 2020 are still here.

The last time I had all six of my recession red flags was late in 2006 and we had a massive consumer credit bubble brewing that set up the great financial recession. But we don’t have that this time.

Yes, history isn’t on our side, but sometimes we create our history as we did with America is back economic recovery model. With some help on the supply side we can have shelter inflation go down, because the best way to fight inflation is to create more supply, not by destroying demand. We have to remember that we have over 900,000 plus two-unit housing under construction that should get online next year which will help with rental inflation.

Then we need the Federal Reserve to get off the Grinch of Christmas theme of causing more pain for Americans by jacking up rates and having banks earn more money on their credit card interest charges. If long bond yields fall, mortgage rates will fall with them like it has since 1971.

If that happens and mortgage rates can get toward 5%, then the housing market can find some stabilization and the bleeding can stop. So, we do have a way to avoid a recession, and even though history isn’t on our side at this stage of the economic expansion, we can connect the dots here and chart a path that avoids more pain.

------------Read More

By: Sarah Wheeler

Title: Can we still avoid a recession?

Sourced From: www.housingwire.com/articles/can-we-still-avoid-a-recession/

Published Date: Mon, 28 Nov 2022 21:38:13 +0000

Did you miss our previous article...

https://trendinginbusiness.business/real-estate/a-historic-home-with-a-contemporary-twist-lists-for-22m-in-los-angeles