.png)

The month of December typically has the lowest weekly seasonal demand for housing, but it’s a big key to how the spring of 2026 will perform — if you know what housing data lines to focus on.

Traditionally, I wouldn’t care so much about December housing data; however, post-COVID, the forward-looking seasonal demand data has started earlier than normal. For example, in the last decade, I would only really value purchase apps during the second week of January to the first week of May, but post-COVID, the November and December data have a strong seasonal push, even when mortgage rates are elevated.

Given that, here’s what you should be looking at in the last month of the year.

Key data lines to track

Despite being a slow month for the housing market, December can give us a good idea of what to expect in the 2026. Let me explain with an example. Back in November of 2022, we were experiencing the most significant and fastest home sales crash ever — so much so that I even said it looked like existing home sales were heading toward 4 million, when they had had only recently dropped a tad under 5 million. As you can see in the chart below, the crash was epic and happened in just one year.

Then, starting from Nov. 9, 2022, mortgage rates began to fall toward 6%, fueling 12 weeks of positive forward-looking data. Those 12 weeks gave us one of the largest monthly sales prints in American history; almost 500,000 more homes were bought in February of 2023. So for the next four weeks, regardless of what the holidays do to the data, we have metrics we can track to give us a sense of how the start of 2026 will look, since mortgage rates are near 6% today. Below are the data lines you should focus on in the month of December.

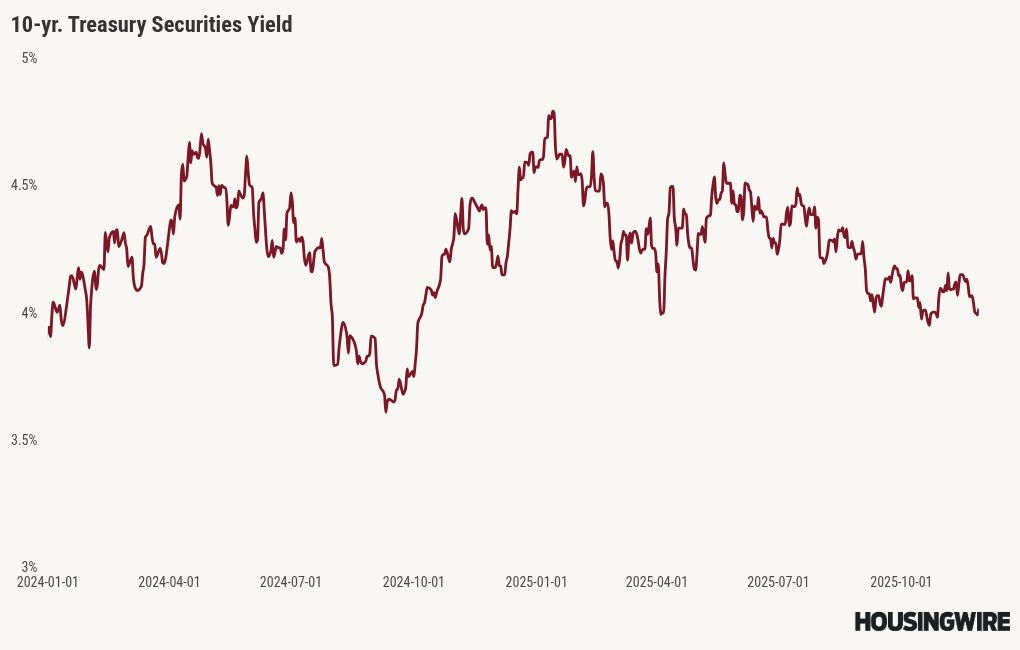

Mortgage rates and the 10-year yield

In my 2025 forecast, I anticipated the following ranges:

- Mortgage rates between 5.75% and 7.25%

- The 10-year yield fluctuating between 3.80% and 4.70%

Mortgage rates are near the lowest levels of the year because the labor data has gotten softer and the Fed was forced to cut rates. As you can see in the chart below, the 10-year yield is close to the year-to-date lows; this wasn’t the case last year at this time. So, as long as the 10-year yield stays near 4% in December, we will have lower rates going into 2026 than we had in 2024 and 2025.

One thing that can change mortgage rates is the upcoming December Fed meeting. Fed Chair Jerome Powell and the other Fed hawks tend to get very hawkish when mortgage rates are near 6%, fearing that more Americans will buy homes. In the last meeting, when the Fed cut rates, Powell sounded very hawkish, hoping bond traders would push yields higher, and they did a bit.

The market is pricing in another rate cut at the December meeting, so the important thing is to listen to what Powell says, because mortgage rates could go higher in December if he is very hawkish. This will be his last meeting before Trump announces the next Fed Chairman near Christmas. However, as long as the 10-year yield is near 4%, mortgage rates will stay near 6%. Also, in 2026, some ARM loans will drop under 6%, something that wasn’t available for Americans in the past few years.

Mortgage spreads

Mortgage spreads were the unsung superheroes of the housing sector this year, because we wouldn’t have had mortgage rates near 6% without them improving. Now, the big difference from the past few years is that the spreads are noticeably better and almost back to normal. As long as this stays true, it will be a plus for 2026, which is why we track this data line each weekend.

Historically, mortgage spreads have ranged between 1.60% and 1.80%. If today’s spreads were as bad as they were at the peak of 2023, mortgage rates would currently be 0.91% higher. Conversely, if the spreads returned to their normal range, mortgage rates would be 0.59% to 0.39% lower than today’s level, meaning mortgage rates would be 5.63%-5.83%.

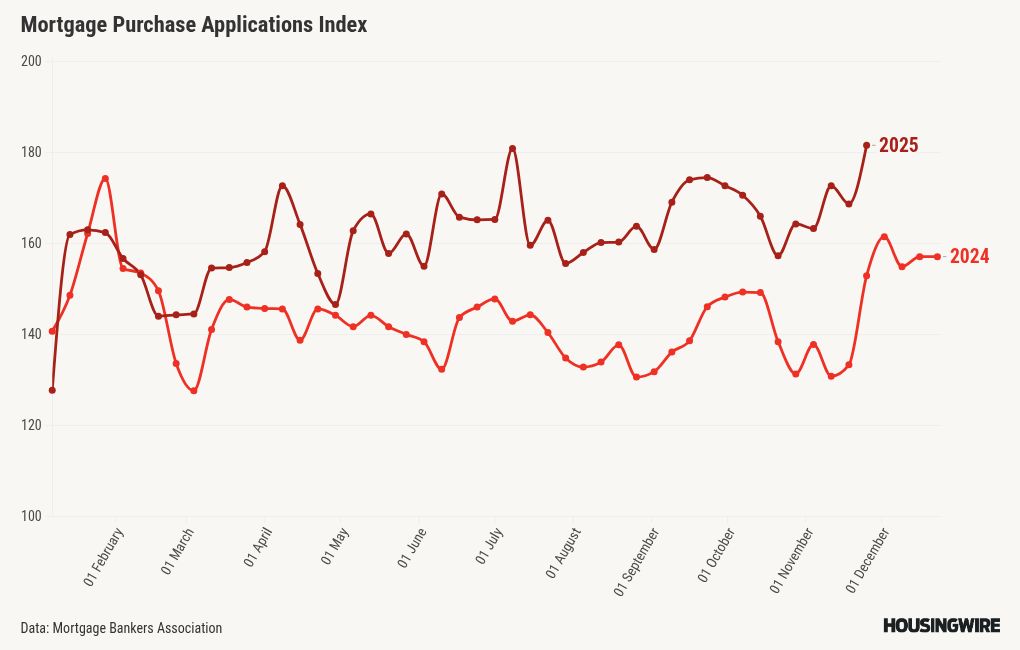

Mortgage purchase application data

Since late 2022, whenever mortgage rates fall below 6.64% and approach 6%, housing data tends to improve, especially in positive weekly purchase application data.

If we can achieve 12 to 14 weeks of positive weekly data, we will establish a solid trend. So far in 2025, we have recorded 10 positive weekly purchase application data prints since mortgage rates dropped below 6.64% at the end of July. Here’s what the data looks like since rates fell below that key threshold:

- 10 positive week-to-week prints

- 7 negative week-to-week prints

- 17 weeks of double-digit year-over-year growth

Here is the data for the entire year. While we have had solid year-over-year growth in purchase apps, the weekly data improved in terms of consistency when mortgage rates fell below 6.64%. For the month of December, we want to continue the positive purchase application trend since last week we hit a year-to-date high in purchase apps.

- 22 positive readings

- 18 negative readings

- 6 flat prints

- 43 straight weeks of positive year-over-year data

- 30 consecutive weeks of double-digit growth year over year

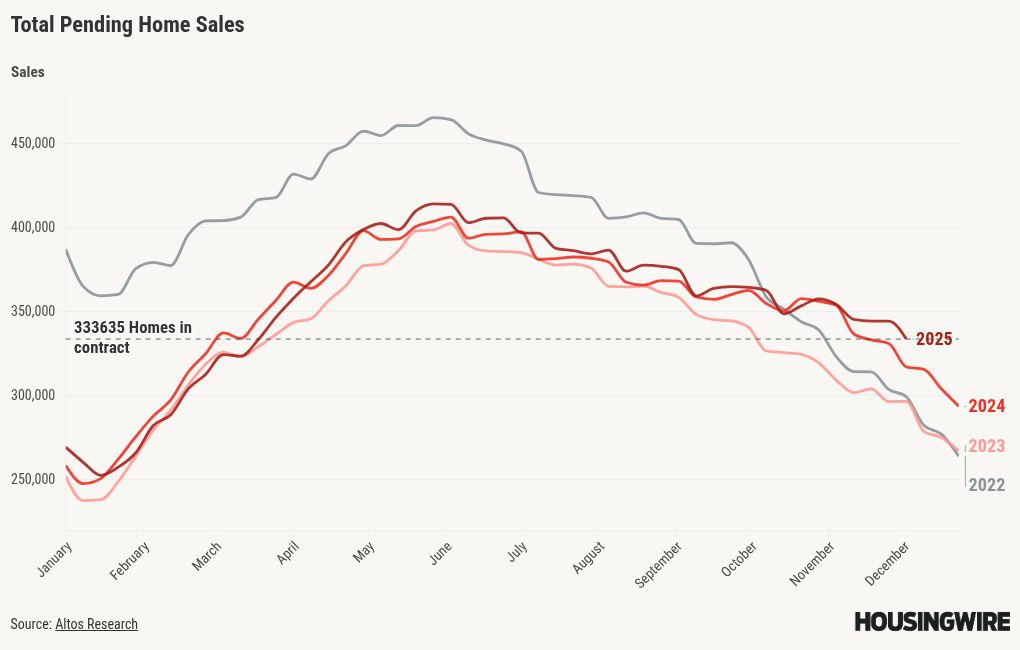

Our total pending sales data below is more positive now than in prior years. As long as mortgage rates stay near 6% and purchase application data grows week to week and year over year, we should see growth in 2026.

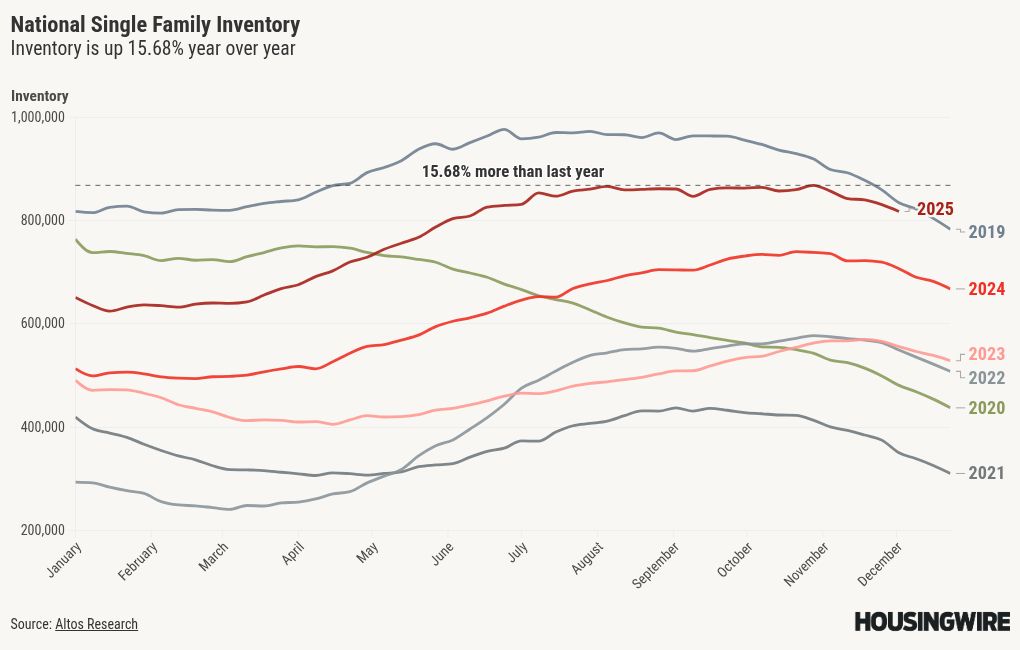

Housing inventory

We are no longer experiencing inventory shortages like we did from 2020-2024 and we’re close to normal inventory levels. Home-price growth is slowing and homebuyers in 2026 will have more options. Sellers do not have the same control they once had during the savagely unhealthy housing market following COVID.

Although we can expect the normal seasonal declines in inventory, new listings and price cuts, the positive story of higher inventory will persist throughout December, so this portion of the story is already written, as the chart below shows.

Conclusion

As we prepare for the last month of the year and the holiday season, it’s essential to monitor forward-looking housing data. You don’t want to be caught unaware, as many were in late 2022, when forward-looking housing data was improving but few were paying attention. It took about six months for people to realize that the market had shifted, as Sarah and I discussed in this 2023 podcast.

For the rest of the year, the key is the 10-year yield and purchase apps. If mortgage rates stay near 6% and purchase apps grow week to week as well as year over year, it’s a good start for 2026 as purchase apps look out 30-90 days and housing acts much better with rates near 6%.

------------Read More

By: Logan Mohtashami

Title: December housing data provides early signals for 2026 market

Sourced From: www.housingwire.com/articles/december-housing-trends-2026/

Published Date: Sat, 29 Nov 2025 23:31:25 +0000

Did you miss our previous article...

https://trendinginbusiness.business/real-estate/my-house-how-finnish-design-shops-marketing-director-decorates-his-450squarefoot-apartment