.png)

The housing affordability crisis often conjures images of coastal urban cities with acute housing supply shortages and heavy land-use regulations. While these places do tend to have the highest home prices, it’s not where costs are rising the most.

That’s according to a sprawling new study from JPMorgan Chase that examines affordability from a number of different angles, with a particular focus on millennials and the post-pandemic era.

Here are three key takeaways from the report.

The pandemic flight to affordability made housing less affordable

Throughout the 2010s, major employers concentrated in urban coastal cities. Part of this effort was to attract millennial workers who want to have the amenities of living in a big city.

But the pandemic reversed that trend — at least temporarily — and now millennials are seeking more affordable areas in smaller metro areas. Texas, Florida, Arizona and parts of the Midwest are some of the places that have seen an influx of residents and resulting home-price gains.

Since the pandemic, home prices have seen the most growth in smaller metropolitan areas and generally outside urban cores. Metros with a population between 500,000 and 1 million have experienced the most price appreciation — and while incomes have also risen substantially, they haven’t kept pace with prices.

In these smaller metros, rural areas (+51.3%), suburban areas (+55.3%), urban areas (+55%) and urban cores (+55.2%) all saw substantial home-price gains over the past five years. Incomes in these areas rose by roughly 38% to 41% during the same period, according to JPMorgan Chase.

Conversely, in metros with more than 5 million people, rural and suburban areas led the way for price growth. At the same time, income growth has outpaced home-price growth in these same areas.

Mortgage rates, not home prices, are fueling the affordability crisis

Household budgets are getting crunched like never before due to rising housing costs.

JPMorgan compared median incomes with housing costs at the start of the pandemic through the end of 2024. It found that homeowners today spend roughly 45% more of their income on mortgage payments.

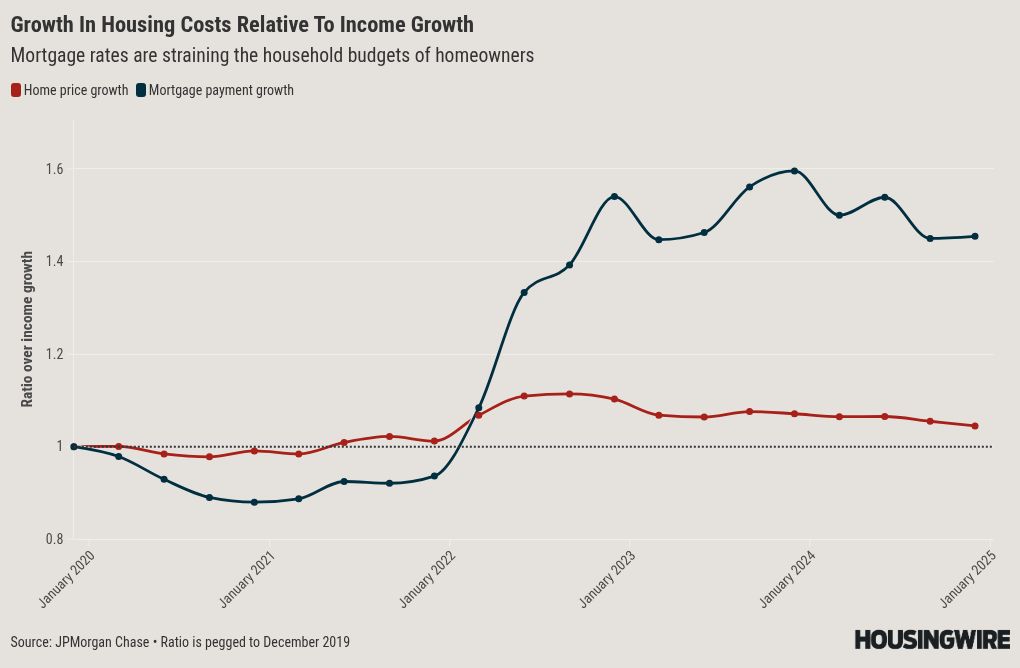

While home prices are rising, mortgage rates near 7% are the primary affordability constraint. The study separately measured home prices and mortgage payments relative to income growth by calculating ratios of home-price growth to income growth and mortgage payment growth to income growth.

It measured these ratios over time and benchmarked them in December 2019. A ratio above 1 means that price growth or mortgage rates are outpacing income growth.

At the beginning of the pandemic, home prices began to rise relative to income growth, but mortgage payments dropped to a ratio of 0.88, meaning that income growth was outpacing growth for mortgage payments.

But that changed dramatically starting in 2020, as both home prices and mortgage rates skyrocketed. The ratio of mortgage payment growth to income growth reached a peak of 1.6 and sat at 1.45 at the end of last year.

Conversely, the ratio of home-price growth to income growth peaked at 1.11 in the fall of 2022 and is now at 1.04. This strongly implies that the current affordability challenges are primarily related to mortgage rates.

Lack of retail investing in the 2010s hurt efforts to save for down payments

First-time homebuyers often use stock market gains to make their down payment, but many millennials didn’t have that advantage.

Stock markets tanked in the aftermath of the 2008 financial crisis and were slow to recover. Many in the millennial generation viewed investing with suspicion and homeownership as potentially risky.

Those who acted according to those sentiments missed out. JPMorgan estimated that the S&P 500 grew threefold over the course of the 2010s. But the share of retail investors in the 25-to-44 age bracket from 2014 to 2019 was substantially lower than from 2019 to 2024.

Unsurprisingly, there were fewer investors at lower income levels, meaning that first-time buyers with moderate incomes, in particular, missed out on a chance to capitalize on stock market gains and potentially fund a down payment.

------------Read More

By: Jeff Andrews

Title: The pandemic made housing less affordable, but not in the obvious places

Sourced From: www.housingwire.com/articles/housing-affordability-crisis-pandemic-jpmorgan-chase-millennials-mortgage-rates/

Published Date: Tue, 17 Jun 2025 20:53:02 +0000