.png)

Mortgages punched through the 7 percent threshold this week on expectations of further Fed tightening but showed signs of easing Friday on speculation that policymakers might slow the pace of rate hikes in December.

The Optimal Blue Mortgage Market Indices, which are updated daily but lag by a day, show rates for 30-year fixed-rate conforming loans breaching 7 percent Wednesday and hitting a new 2022 high of 7.1 percent on Thursday.

Yields on 10-year Treasury bonds, a barometer for mortgage rates, also hit a new 2022 high Friday before retreating after The Wall Street Journal detailed concerns some Fed policymakers have voiced about the relentless pace of rate hikes.

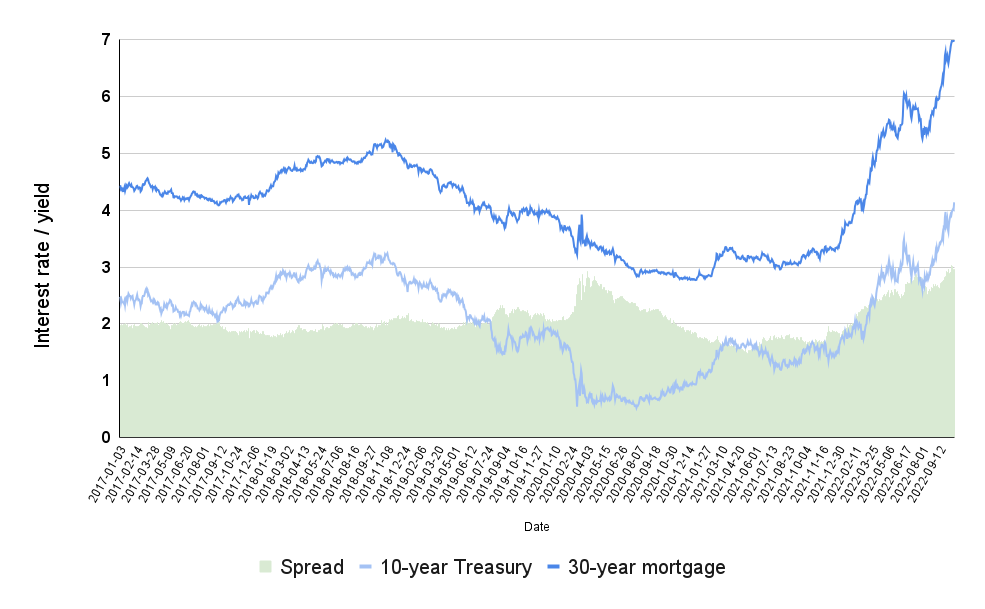

Mortgage rates’ relentless climb

Another daily rate index compiled by Mortgage News Daily shows mortgage rates retreating slightly from Thursday to Friday.

The Federal Open Market Committee, which sets short-term interest rates, has raised the short-term federal funds rate five times this year. Although Fed policymakers started with a 25-basis point increase in March, they quickly escalated the pace of rate hikes to 50 basis points in May and 75 basis points in June, July and September, having seen few signs that inflation is moderating.

While another 75-basis point increase in the federal funds rate on Nov. 2 is seen as inevitable, bond market investors who fund most mortgages are now focused on the committee’s Dec. 14 meeting.

The CME FedWatch Tool, which monitors futures contracts to calculate the probability of Fed rate hikes, puts the odds of a 75-basis point increase in November at 92 percent. But futures markets put the odds of another hike of the same magnitude in December at less than half.

Several Fed policymakers have hinted that they’d be open to a smaller 50-basis point increase in December if there are signs that inflation is starting to ease. Those policymakers include Fed Vice Chairwoman Lael Brainard, Chicago Fed President Charles Evans and Kansas City Fed President Esther George, The Wall Street Journal’s Nick Timiraos reported.

But “dovish” policymakers who might favor a less aggressive approach “are in the penalty box” and will have a hard time convincing their more hawkish colleagues to back off, as they’ve been wrong about inflation “at key turning points over the last 18 to 24 months,” Renaissance Macro Economist Neil Dutta told Timiraos.

“I imagine we will have a very thoughtful discussion about the pace of tightening at our next meeting,” Fed governor Christopher Waller said in an Oct. 6 speech at the University of Kentucky.

“While housing seems likely to continue contributing to high inflation in the near term, in the medium-term higher mortgage rates should slow the housing component of inflation as housing demand cools,” Waller said. But for now, he said, “I anticipate additional rate hikes into early next year, and I will be watching the data carefully to decide the appropriate pace of tightening as we continue to move into more restrictive territory.”

Fed policymakers will pay close attention to an upcoming report on worker compensation, the Employment Cost Index (ECI), to be released on Oct. 28, Timiraos reported.

“The market is torn between those who hope the worst will soon be in the past and those who believe the Fed will tighten policy further at a time when the strong dollar is increasing global tensions,” Reuters reported, citing RBC Global Asset Management’s Andrzej Skiba.

“We’re not sure that relatively strong economic data and elevated inflation will allow them to [slow the pace of rate hikes] in the near term,” Skiba told Reuters.

Jared Bernstein, an economist who’s a member of the White House Council of Economic Advisers, tweeted Friday that he sees signs that “Supply chains are unsnarling and this is taking some pressure off of inflation.”

A Mortgage Bankers Association survey showed demand for home loans last week hit the lowest level since 1997 as rates continued to rise.

In a research note, Pantheon Macroeconomics Chief Economist Ian Shepherdson agreed that the abrupt rise in mortgage rates will hurt home sales, but that a recession is not inevitable.

“The plunge in demand is now pushing home prices down, despite very low inventory of existing homes. But inventory of new homes is high, and when homebuilders cut prices, private sellers have to follow,” Shepherdson wrote. “We think prices will fall by 15 to 20 percent from their peak by the middle of next year. Housing and related activity account for less than 10 percent of GDP, so the housing sector — like manufacturing — can be in recession while the rest of the economy is not. The current housing shock is nothing like 2006-to-10, given the absence of resetting adjustable rate mortgages and the lack of housing equity withdrawal in recent years.”

If the Fed’s efforts to combat inflation do lead to a recession, interest rates are likely to come back down, giving many homeowners taking out loans today the opportunity to refinance at a lower rate.

Widening ‘spread’ between Treasurys and mortgages

Source: Inman analysis of data from Board of Governors of the Federal Reserve System (10-year Treasury yields) and Optimal Blue Mortgage Market Indices (30-year fixed-rate conforming mortgages) | Data retrieved from FRED, Federal Reserve Bank of St. Louis

That’s one factor driving mortgage rates up even faster than yields on 10-year Treasurys, Moody’s Analytics Chief Economist Mark Zandi noted last month. The “spread,” or difference between 10-year yields and 30-year mortgage rates has averaged 2.05 percentage points in recent years.

That spread has widened this year, exceeding 3 percentage points at times during October, reflecting mortgage investors’ fears of prepayment risk.

This article was written by Matt Carter from Inman News and was legally licensed through the Industry Dive Content Marketplace. Please direct all licensing questions to [email protected].

Read More

By: admin

Title: Mortgage rates punch through 7% but may pause for Fed clues

Sourced From: www.pncrealestatenewsfeed.com/mortgage-rates-punch-through-7-but-may-pause-for-fed-clues/

Published Date: Mon, 24 Oct 2022 17:43:56 +0000