.png)

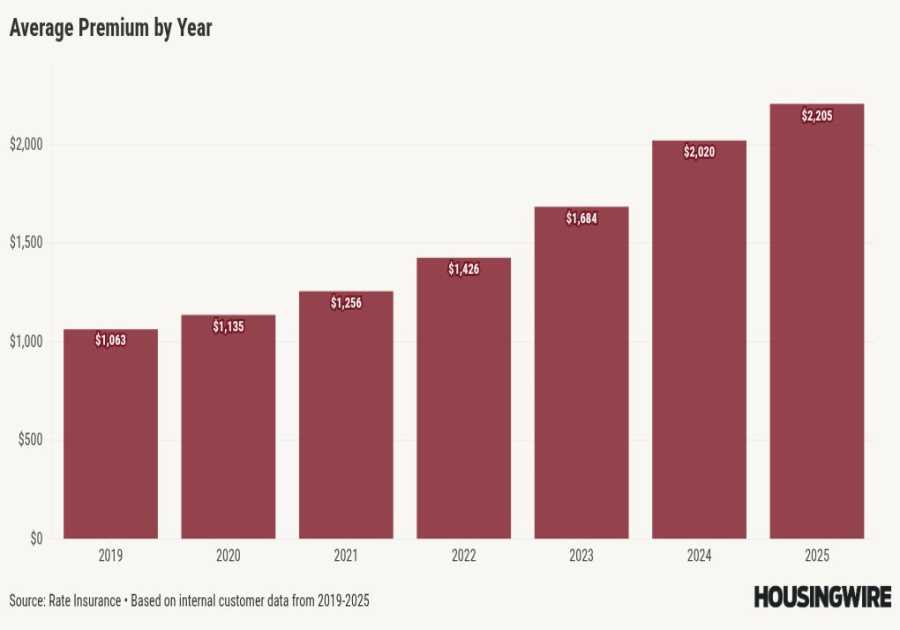

Homeowners insurance premium growth slowed in 2025 after several years of steep increases, but coverage costs have still more than doubled since 2019, according to a new report released Thursday by Rate Insurance, a subsidiary of Rate.

The company’s 2026 Home Insurance Trends Report found that the average homeowners insurance premium in its portfolio rose 9.16% in 2025, increasing from $2,020 to $2,205. That marked the first notable slowdown since 2019 after annual increases approaching 20% in 2023 and 2024.

Even with the moderation, average premiums have climbed 107.6% over the past six years, far outpacing the growth in dwelling coverage limits, which rose 45.6% during the same period, the report said.

“After several years of sharp increases, we’re starting to see early signs that the market is stabilizing,” said Jeff Wingate, president of Rate Insurance. “Premiums are still elevated, but this shift gives homeowners a window to reassess their coverage, make informed adjustments and take a more proactive approach to managing long-term costs and their overall financial well-being.”

The report analyzed more than 265,000 homeowners policies placed with 100-plus carriers nationwide, as well as more than 7,500 claims filed between 2018 and 2025.

Insurance costs varied sharply by state. Colorado had the highest average annual premium in Rate Insurance’s portfolio at $3,392, followed by Texas at $3,343, Oklahoma at $3,135 and Florida at $2,946. Washington, D.C., had the lowest average premium at $1,197.

Maine posted the largest year-over-year price increase in 2025 at 21.37%, while Florida saw one of the smallest increases among larger states at 4.4%.

The report also found widening gaps between premiums and replacement costs. Average estimated replacement costs reached $478,000 in 2025, up more than 40% over five years. Meanwhile, the average national cost of coverage rose to $4.61 per $1,000 of replacement cost, compared with $3.24 in 2019.

Oklahoma recorded the highest cost per $1,000 of replacement value at $9.83, followed by South Dakota and Florida. Washington, D.C., Vermont and Oregon had the lowest costs.

Higher deductibles are also becoming more common as insurers shift more risk to homeowners. The share of policies with deductibles under $2,500 fell to 59.67% in 2025, compared to 73.52% in 2018, while policies with deductibles of $2,500 to $10,000 saw their share rise to nearly 40%.

In Louisiana, more than 85% of Rate Insurance customers carried deductibles of at least $2,500, according to the report.

Many policies also include percentage-based wind or hail deductibles, which can leave homeowners with large out-of-pocket costs after severe storms. A 5% deductible on a $400,000 home, for example, would require the homeowner to pay $20,000 before insurance coverage begins.

Claims data in the report showed fewer claims filed overall but higher claim severity. Total claims dropped to 1,045 in 2025, down from a peak of 1,704 in 2023. But the average claim severity increased to $32,600, compared to $24,600 a year earlier.

The report attributed much of the increase to the January 2025 California wildfires, including the Eaton and Palisades fires. Fire and lightning claims represented less than 5% of total claims in 2025 but accounted for nearly half of all claim dollars paid.

Water and freezing damage remained the most common claims category, accounting for more than half of claims over the past five years.

The report also highlighted growing scrutiny of roof conditions by insurers, which increasingly use satellite imagery and artificial intelligence to evaluate properties. Carriers are more frequently limiting coverage, increasing premiums or shifting homeowners to actual cash value roof coverage for older roofs.

That trend coincides with a March 2026 policy change by the Federal Housing Finance Agency (FHFA), allowing Fannie Mae and Freddie Mac to accept policies with actual cash value roof coverage instead of requiring full replacement cost coverage.

Rate Insurance said homeowners should use the recent slowdown in premium growth to review coverage limits, deductibles and rebuilding costs, especially in areas vulnerable to natural disasters.

This article was generated using HousingWire Automation and reviewed by a HousingWire editor before publication. The system helps convert company announcements and industry data into HousingWire-style news coverage.

------------Read More

By: HousingWire Automation

Title: Rate Insurance: Home premiums rose 9% in 2025

Sourced From: www.housingwire.com/articles/homeowners-insurance-2025-rate/

Published Date: Thu, 21 May 2026 15:36:22 +0000

Did you miss our previous article...

https://trendinginbusiness.business/real-estate/fearless-at-foreclosure-auction