.png)

Mortgage rates have been a bit more volatile recently due to hawkish Federal Reserve statements and inflation data, which has impacted some of the recent movement in the 10-year yield. But now we have the big jobs week coming up! So, what does this all mean for the housing market and the future of mortgage rates?

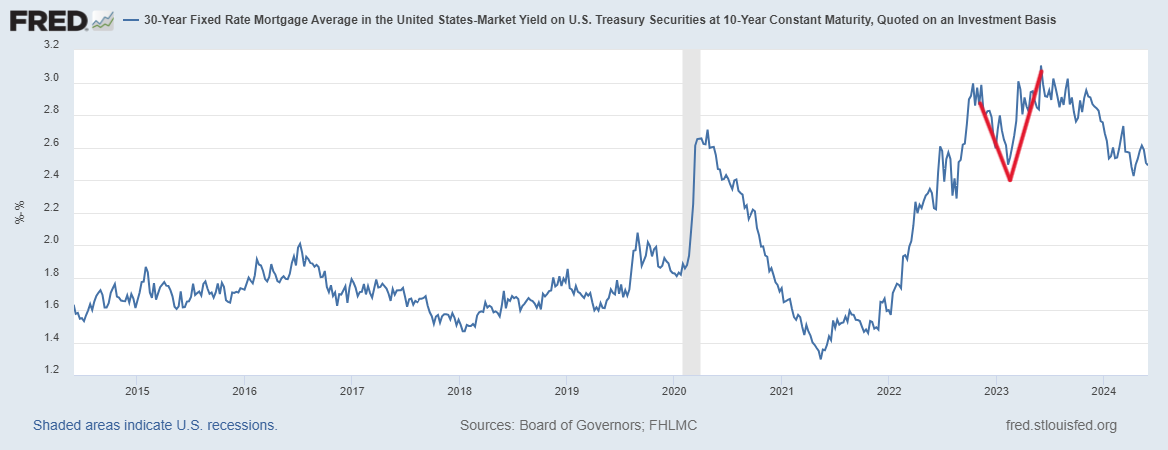

10-year yield and mortgage rates

As we approach a crucial week for mortgage rates, the 10-year yield and labor data could influence the Fed’s decisions. If we witness more softness in the labor market, the 10-year yield and the labor data will eventually force the Fed’s hand. However, the Fed wouldn’t mind seeing mortgage rates lower when the labor market breaks. Last week, we saw some volatility in the 10-year yield, but after the mild miss in the inflation data Friday, the 10-year yield closed the week at 4.50% and mortgage rates ended the week on a positive

positive note.

Mortgage spreads

The spread between the 30-year mortgage rate and the 10-year yield has been terrible for a prolonged period. This is particularly frustrating since it’s the third calendar year with the lowest home sales ever, especially when adjusting to the workforce. However, the spreads have been getting better this year compared to last year.

If we took the worst levels of the spreads from the previous year and incorporated those today, mortgage rates would be roughly 0.60% higher today. So, as frustrating as the spreads can be, they are much better than last year. If the spreads return to normal, we could see a 0.75% to 1% improvement in mortgage rates just from that — without the 10-year yield moving lower.

Purchase application data

The seasonality of purchase application data ended last week, as volume typically starts to fall after May. However, the mortgage purchase application data is so low historically on the volume side that the seasonal drop can be limited. Also, if mortgage rates drop again by 1% as they have in the previous two years during the fall, we can get a bounce in purchase apps.

Since November 2023 when mortgage rates started to fall, we have had 12 positive prints versus 12 negative prints and two flat prints week-to-week. Once mortgage rates began rising in 2024, some demand was removed. As we can see below, the year-to-date data isn’t even positive for 2024. So far, in 2024, we have had 6 positive prints, 12 negative prints, and two flat prints.

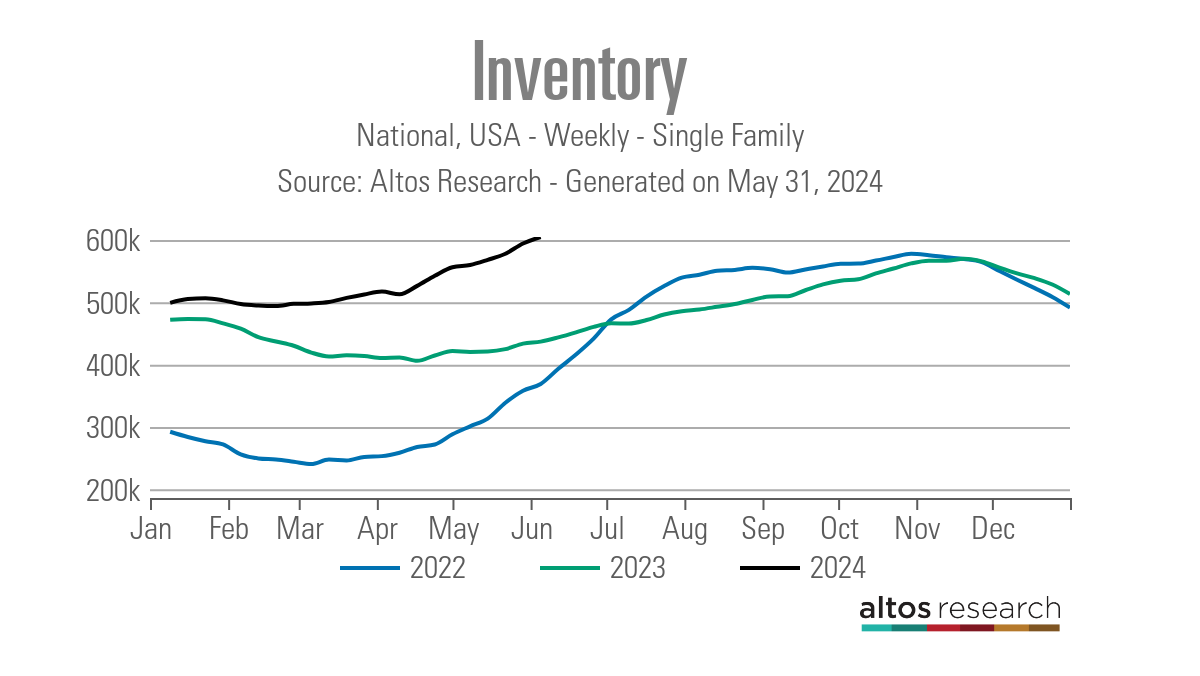

Weekly housing inventory data

The best story about housing in 2024 has been that we are finally growing inventory and getting off these savagely unhealthy low levels of active listings. You can hear more about this in our recent HousingWire Daily podcast. Even though we didn’t hit my goal this week of inventory growth between 11,000 – 17,000, it was still a decent week at 10,374.

it was still a decent week at 10,374

- Weekly inventory change (May 24-May 31): Inventory rose from 594,548 to 604,922

- The same week last year (May 26-June 2): Inventory rose from 433,838 to 437,007

- The all-time inventory bottom was in 2022 at 240,194

- This week is the inventory peak for 2024 at 604,922

- For some context, active listings for this week in 2015 were 1,132,726

New listings data

New listings data has been showing positive year-over-year growth all year, which is a big plus for housing since most sellers are buyers. This week, the data did dive, but it was the traditional drop we see during the Memorial Day weekend and we will have a rebound in the data line next week. We are near the seasonal decline for this data line, and if we don’t hit at least 80,000 this year, I will be disappointed. Remember that even though we are showing growth year over year — 2023 was the lowest levels of new listings ever recorded in history.

Here’s the new listing data for last week over the previous several years:

- 2024 63,465

- 2023: 54,723

- 2022: 70,272

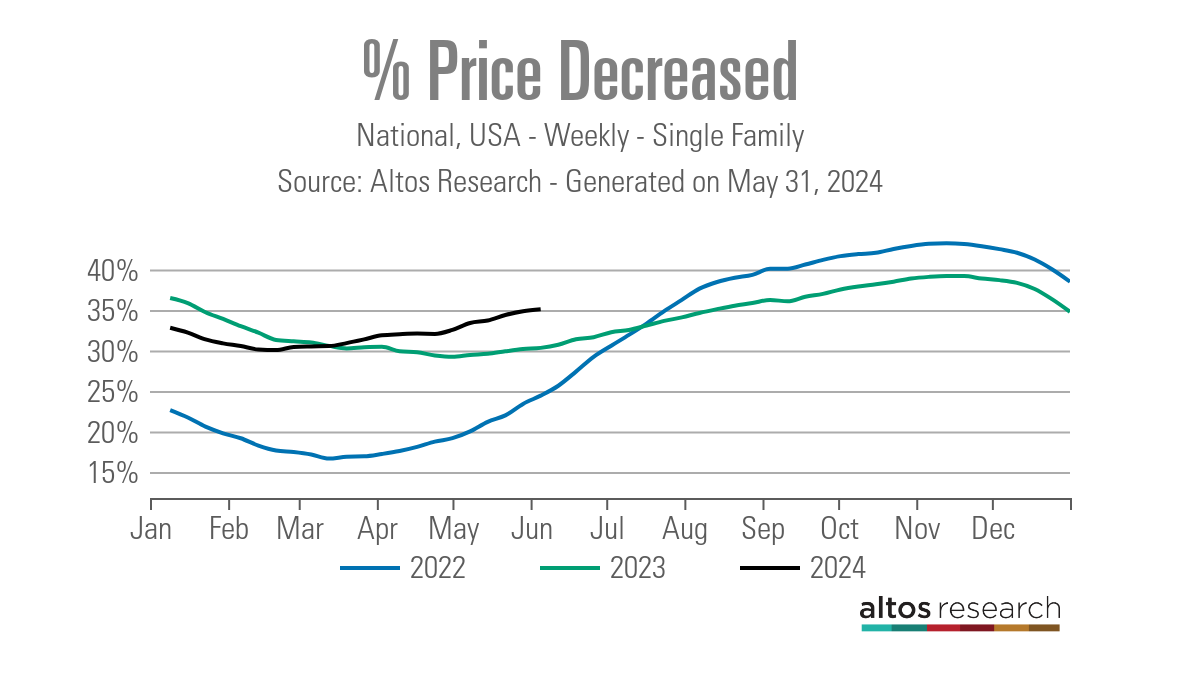

Price-cut percentage

In an average year, one-third of all homes take a price cut — this is standard housing activity. When mortgage rates increase, demand falls, and the price-cut percentage grows. When rates drop, and demand improves, price cut percentage can fall. This data line is very seasonal, and we have seen consistent year-over-year price cut percentage growth since the end of March.

This is one of the reasons we will see a cooling in home prices from the start of the year. I recently talked about this in our podcast and explained why I believe this to be the case. Here are the price cut percentages for last week over the last few years:

- 2024: 35%

- 2023: 30%

- 2022: 24%

The week ahead: JOBS WEEK!

It’s a big week for housing with reports on the labor market, the economy and mortgage rates. On Monday’s podcast, I will discuss a bit more why the labor data is so important this week but also going out for the rest of this year and 2025 since we are in a different part of the economic cycle today versus a year ago.

We have job openings, ADP jobs reports, jobless claims and the big Jobs Friday report to look forward to this week. After a lighter-than-anticipated inflation report, mortgage rates can head lower if we see multiple soft labor reports. One thing to remember with the labor data is that it’s no longer a tight labor market, but it hasn’t broken yet. It’s very key to track all labor data to know when it breaks because it will have big implications for the housing market and mortgage rates.

------------Read More

By: Logan Mohtashami

Title: This is a big week for housing, jobs and mortgage rates

Sourced From: www.housingwire.com/articles/this-is-a-big-week-for-housing-jobs-and-mortgage-rates/

Published Date: Sat, 01 Jun 2024 22:09:45 +0000

Did you miss our previous article...

https://trendinginbusiness.business/real-estate/a-fatherandson-construction-team-try-their-hand-at-tiny-homes