.png)

Recent mergers and acquisitions (M&A), regulatory changes and shifting market conditions have mortgage industry experts questioning whether servicers are better positioned than other competitors to capture the next wave of refinances.

Data from ICE Mortgage Technology shared with HousingWire offers a deep dive into servicers’ performance at keeping a borrower in their books after a refinance transaction. It shows that, on average, servicers have retained about 30% of borrowers since the second quarter of 2010.

Servicer retention, however, varies with market cycles. And, in the current landscape, competition is expected to intensify as Rocket Companies agreed to acquire Redfin and Mr. Cooper Group, and Bayview Asset Management has proposed a deal for Guild Mortgage.

At the same time, a recent ban on abusive trigger leads — signed into law by President Trump in September — is expected to give servicers and lenders an additional edge by allowing them to contact current customers directly. The rule coincides with mortgage rates falling to their lowest levels in nearly a year, spurring fresh refinance activity.

Beyond market conditions, structural characteristics such as product type, loan vintage, servicer profile and investor backing also shape retention outcomes, according to ICE.

“This report primarily comes out of our MSP servicing system that flows over into what we call our McDash database. It’s like 35 million loans,” Andy Walden, ICE’s head of mortgage and housing market research, said in an interview. “We match that data anonymously to public records.”

Overall retention trends

ICE data shows that servicer retention recently peaked at 33% in Q4 2021, dropped to 20% in Q2 2024, and recovered modestly to 24% in Q2 2025. But servicer retention differs by refinance product.

“When interest rates fall and refinances boom, companies become more traditional, going toward rate-and-term refis,” Walden said. “Lenders and servicers tend to do a better job of retaining borrowers in that environment.”

Rate-and-term refis currently see a 29% servicer retention rate, while cash-out refis lag at 21%. In Q2 2024, when rates were higher, that trend was reversed—cash-outs had stronger servicer retention than rate-and-term transactions.

One caveat: cash-out candidates present challenges because they are harder to identify. But they present opportunities as well. In Q2 2025, 70% of cash-out refinances came from borrowers who accepted higher interest rates — averaging a 1.5 percentage point increase and a $590 higher monthly payment — in exchange for pulling about $94,000 in equity.

“If you’re using traditional ‘in-the-money’ analytics to try to identify borrowers looking to refinance, you’re missing that entire chunk of the market.” Walden said.

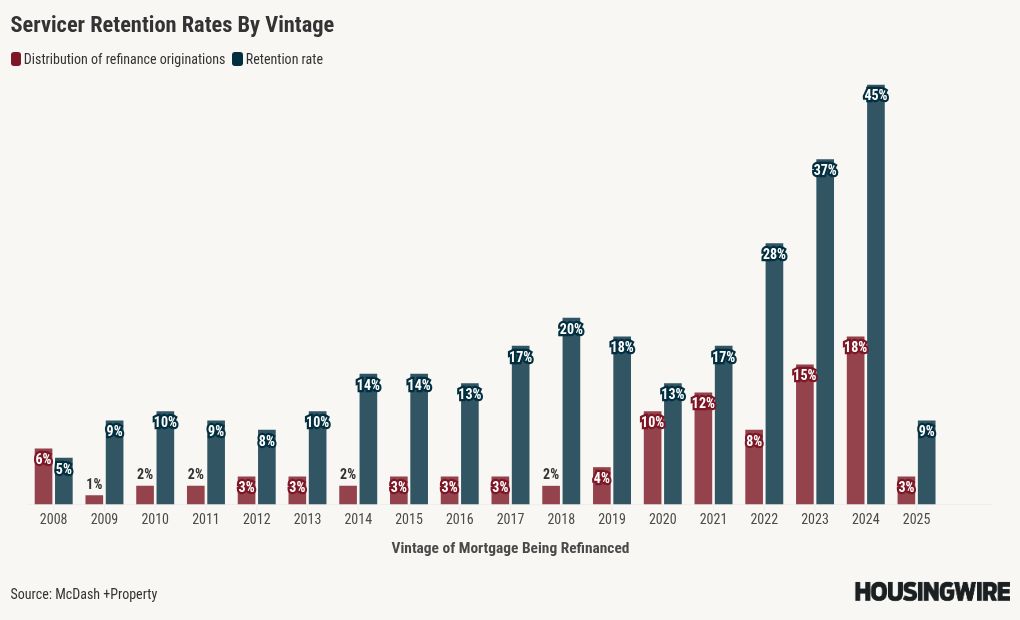

Loan vintage matters

As expected, servicers are most effective at retaining borrowers that have recently originated loans. But the current wave of industry consolidation is also expected to funnel more business to larger players, reinforcing that trend. Walden highlighted both factors as reasons retention rates are highest among the 2024 vintage.

Servicer retention stands at 45% for 2024 loans, dropping to 37% for 2023, 28% for 2022 and just 17% for 2021.

“Part of it is simply the recency of the relationship,” Walden said. “Over the last five to seven years, you always see this downward slope: higher retention for recently originated loans, and lower retention the further away you get.”

The other factor is that many borrowers took out mortgages with the expectation of refinancing as soon as rates dropped, he added.

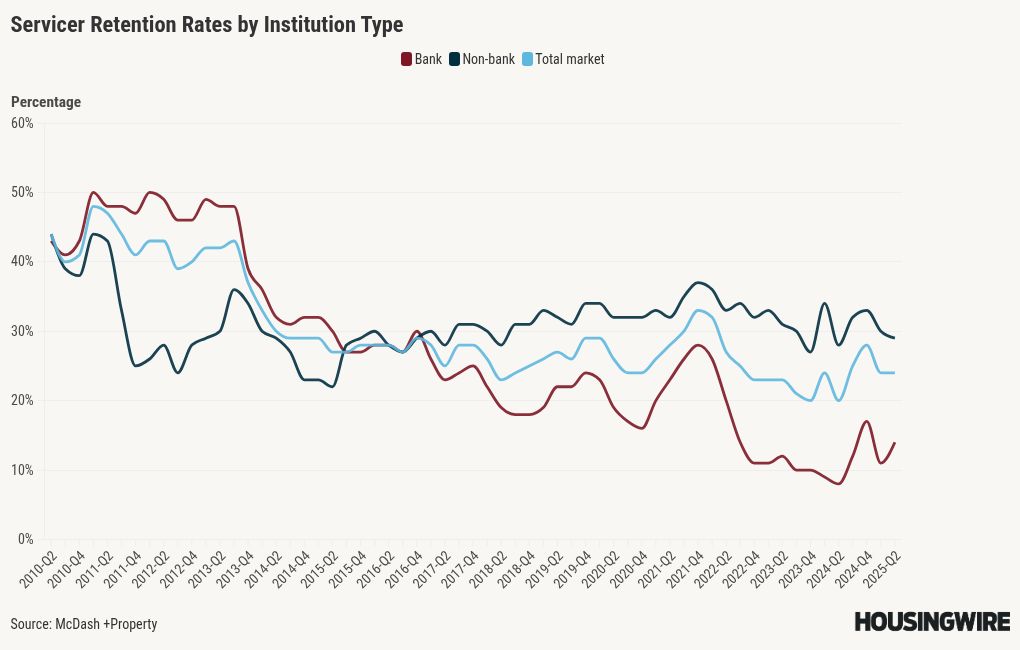

The role of nonbanks

When comparing banks and nonbanks, the latter are far more active, deliberate and successful at retaining borrowers. In Q2 2025, nonbanks posted a 29% retention rate, more than double the 14% rate among depositories.

“Holistically, we know that they’ve been moving away from the servicing space,” Walden said.

According to Walden, banks face much more regulatory pressure, so in many cases — especially in the lower credit score segments of their portfolios — they’re content to let those loans run off to a nonbank. Instead, they focus on retaining higher-wealth clients in areas like home equity or wealth management.”

By size, mid-tier banks retained 22% of borrowers, compared with just 13% at large banks. Among nonbanks, the rate was 29% across the board, regardless of size.

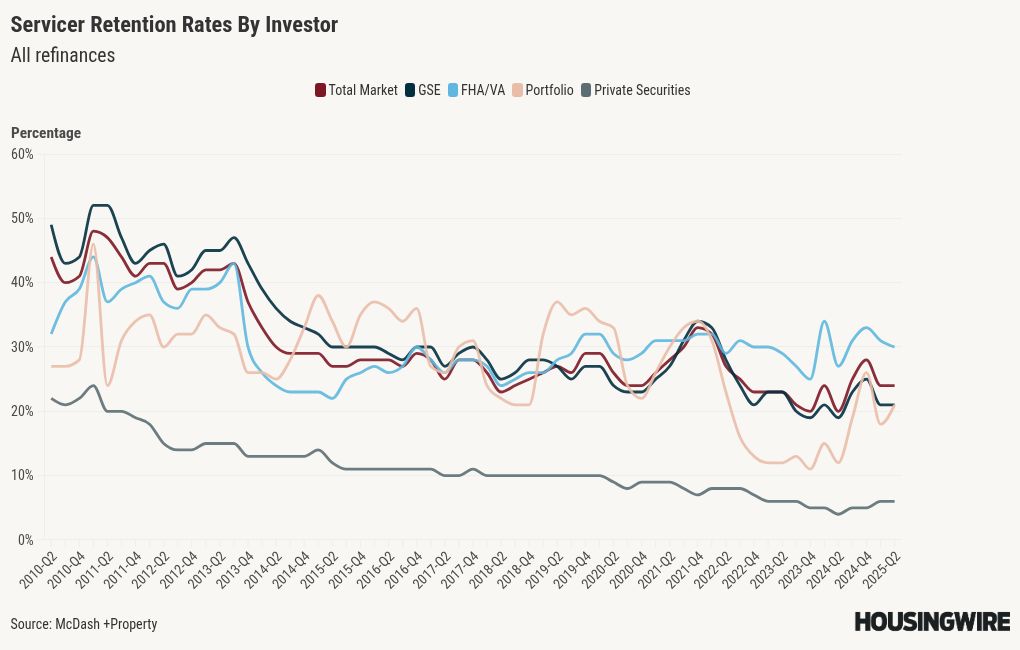

Investor type drives results

Retention rates for servicers vary significantly by investor type. In Q2 2025, Federal Housing Administration (FHA) and U.S. Department of Veteran Affairs (V.A.) loans led with a 30% servicer retention rate, compared to 21% for Fannie Mae and Freddie Mac loans, 21% for portfolio refinances, and just 6% for private-label securitizations.

According to Walden, many of the lower-credit-score loans in private-label securities were originated more than a decade ago, and servicers are often content to let those run off rather than actively retain them.

By contrast, FHA and VA borrowers are seeing heavy outreach. “The rate offerings right now are lower on FHA and VA, and they also have streamlined products,” Walden said. “On the VA side, equity is being used to buy down rates.”

------------

------------Read More

By: Flávia Furlan Nunes

Title: Who keeps the borrower? A deep dive into servicer retention

Sourced From: www.housingwire.com/articles/who-keeps-the-borrower-a-deep-dive-into-servicer-retention/

Published Date: Mon, 29 Sep 2025 19:53:43 +0000