.png)

Eastwood Homes’ acquisition of Atlanta-based Peachtree Building Group – announced today – maps out on its surface as a straightforward expansion move.

Eastwood Homes, our HousingWire Homebuilder Ranking’s No. 11-ranked private homebuilder, is a fast-growing Charlotte-based builder that, with this deal, deepens its Southeastern footprint by adding local scale, operating capability, and market presence in one of the nation’s most strategically consequential housing markets.

But that surface reading clouds a compelling and, likely, more important story in a mergers and acquisitions landscape roiling with motivations, competitive fever and strategic shifting in balances of power.

Broadly, the deal speaks to a current homebuilding consolidation cycle; some of the most consequential buyers are neither Wall Street-backed public giants nor Japan’s globally capitalized housing conglomerates.

They are the increasingly formidable cohort of multi-regional private homebuilders.

Well-capitalized. Operationally disciplined. Strategically ambitious. Often culturally attractive to seller-founders who care as much about legacy, people, and reputation as they do price.

And increasingly active.

According to JTW Advisors, which served as financial advisor to Eastwood Homes on the transaction, private builders accounted for 39% of homebuilder M&A buyers in 2025 through April 2026 — ahead of Japanese acquirers at 30% and public builders at 26%. That’s a dramatic shift from prior cycles, when public builders overwhelmingly dominated acquisition activity.

Eastwood’s move into Atlanta belongs squarely in that trend.

The race for scale isn’t just a public builder imperative

For years, and intensifying during the pandemic and post-pandemic era, homebuilding M&A headlines have tended to cluster around familiar themes. Lennar, D.R. Horton, Toll Brothers, and other publics are pursuing market share. Japan-based operators such as Sumitomo Forestry, Daiwa House, and Sekisui House are making increasingly assertive U.S. bets. Private equity and institutional capital are circling attractive platforms.

All real forces.

JTW’s data makes clear that a broader structural shift is underway.

From 2010 to 2014, private buyers accounted for just 12% of U.S. homebuilder acquisitions. Between 2020 and 2024, that climbed to 25%. In the current 2025-YTD 2026 window, it has jumped to 39%.

That may have been a subtler part of the M&A story, but the forces propelling the trend need to be appreciated to fully discern homebuilding’s power shifts. A growing class of “super-private” builders is reaching the point where scale economies, geographic diversification, talent acquisition, and operational leverage make M&A anything but opportunistic.

Rather, those forces make deals practically competitively necessary.

More data from JTW supports this.

Trailing-12-month SG&A for small-cap builders runs around 13%, versus 10.8% for mid-caps and 8.4% for large caps. EBITDA performance follows the same scale advantage logic.

The translation is simple: size matters more and more, regardless of the underlying capital stack. Heft and clout are high on the list for land deals, supplier priorities, and trade contractors in a market where affordability pressure, consumer hesitancy, incentive costs, land complexity, entitlement risk, insurance volatility, and longer sales cycles punish inefficiency.

Eastwood, under CEO Clark Stewart and CFO Kevin Hutchins, clearly understands that.

“This is an exciting moment for Eastwood Homes,” said Clark Stewart, President of Eastwood Homes, in a prepared release. “Our continued growth is a reflection of the strength and health of our company, as well as the dedication of our team members across every market we serve. We are proud to continue expanding thoughtfully into markets that align with our long-term vision and values.”

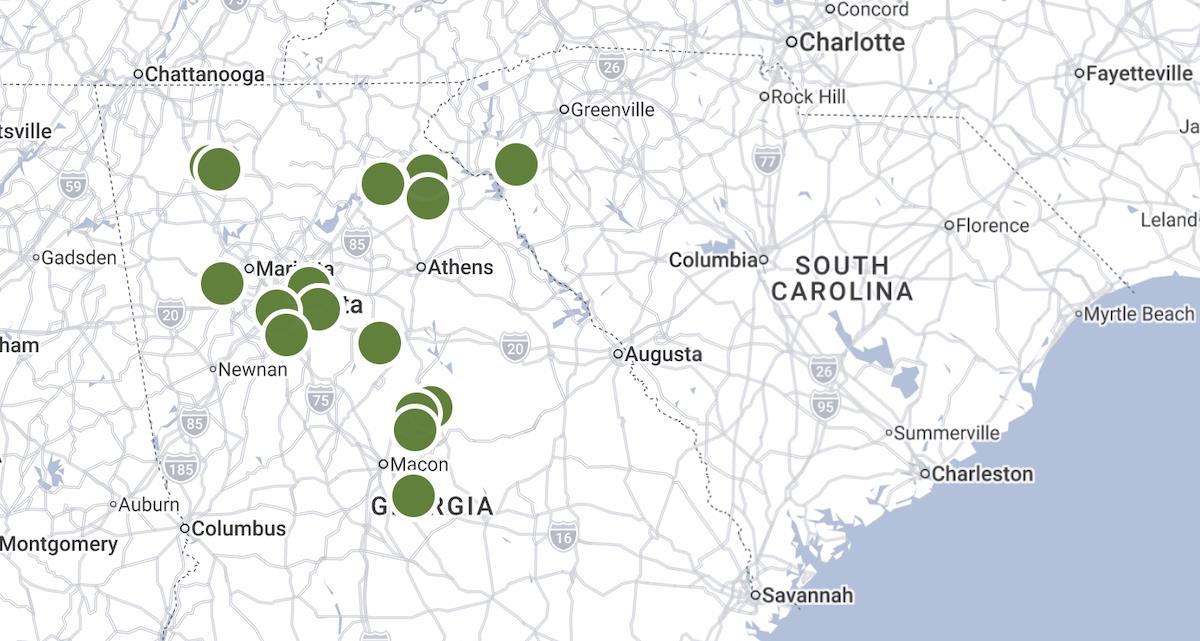

Why Atlanta Matters Now

Atlanta remains one of the most strategically attractive growth markets in American homebuilding.

Population migration, economic diversification, employment growth and relative affordability versus coastal markets continue to make metro Atlanta a magnet for household formation and builder investment.

That’s precisely why KB Home recently moved to establish a deeper Atlanta presence, as ResiClub’s Lance Lambert noted in his analysis of builders chasing demographic momentum and long-term growth markets.

Eastwood was already in Atlanta. But “being in a market” and “having scaled relevance in a market” are two very different realities. This acquisition appears designed to accelerate the latter.

Peachtree Building Group brings more than 35 years of experience, with leadership roots among top-five Atlanta builders and a track record spanning thousands of homes across Southeastern markets.

That matters because Atlanta is not a market where adjacency knowledge alone wins.

- It rewards local execution.

- Land relationships.

- Municipal familiarity.

- Trade partner trust.

- Product-market fit.

- Lot pipeline intelligence.

That’s hard to build organically with enough competitive runway to outperform mega-players crowding one of the nation’s most attractive, fast-growing new-home markets.

Buying the local intelligence, trusted relationships, strong reputation, and proven ability to counterpunch larger, better-capitalized players is often faster – and less risky.

Eastwood’s M&A pattern comes into focus

Eastwood Homes’ acquisition of Peachtree Building Group does not appear to be a one-off geographic land grab. Rather, Eastwood’s growth trajectory and approach suggest deliberate moves within a broader strategic evolution.

When Eastwood acquired Napolitano Homes in the Hampton Roads market last year, the signal was subtle yet clear. The transaction was framed not simply as an expansion play but as a combination built on shared operating values, local reputation and cultural compatibility. Eastwood’s leadership made no secret that alignment between the two organizations’ business philosophies was central to closing the deal.

The Peachtree acquisition broadens that pattern, even if the strategic rationale here is more overtly growth-oriented.

Atlanta presents a very different scale of opportunity than Hampton Roads. This is not merely an adjacency expansion. It is an entry into one of the nation’s most strategically contested housing-growth corridors, where demographic migration, economic diversification, and long-term household-formation trends continue to attract builder investment. Yet even in a market-opportunity-driven deal, Eastwood appears to be following the same disciplined playbook.

The public messaging about the acquisition emphasizes continuity – particularly the preservation of Peachtree’s operating relationships with employees, trade partners and customers.

Sophisticated homebuilding acquirers increasingly understand that the most valuable assets in local private builders are often intangible: market credibility, municipal relationships, trade trust, institutional knowledge, and operating teams that have the know-how to get homes built and delivered in specific local environments.

Those assets can evaporate quickly when integration is handled poorly.

Eastwood’s approach suggests a buyer who understands that it is not simply purchasing lots, backlog, revenue or a bigger pipeline to homebuying customers. It is acquiring local operating capability that took decades to build.

That’s the difference between strategic acquirers and financial opportunists.

Why sellers like Peachtree enter deals like this

No public explanation has been offered for why Peachtree’s ownership chose this moment to sell. But the broader market context offers more than enough explanation.

Running an independent homebuilding business has become materially harder and materially more tilted in favor of those with access to more patient, less expensive operating, land investment, and construction capital.

The cost of capital remains elevated relative to the era when many private builders developed their expansion strategies. Land competition has intensified. Entitlement complexity continues to slow development cycles. Customer acquisition costs have risen sharply in an environment where buyers are more hesitant, more payment-sensitive and harder to convert.

Insurance risk has introduced new uncertainty into underwriting projects and communities. Entitlement risk can ensnarl land parcels for weeks, months, or longer, tying up capital and weighing on loan covenants. Sales velocity can shift quickly, while cash conversion cycles are lengthening.

Bottom line, scale increasingly confers advantages that smaller operators cannot easily replicate.

Purchasing leverage improves with scale. Overhead is spread more efficiently. Technology investments become more rational. Talent recruitment becomes easier. Geographic diversification helps cushion local shocks.

For founder-led private operators, that creates a stark strategic question: continue competing independently against increasingly industrialized rivals, or join forces with an acquirer whose resources improve the probability of long-term success.

“This transaction reflects the continued strength of the homebuilding M&A market, particularly among well-positioned operators pursuing strategic expansion opportunities,” said Chris Jasinski, Founder & CEO of JTW Advisors. “Eastwood Homes has built an impressive business and reputation over multiple generations, and we are honored to advise them on this acquisition.”

Importantly, not every seller views the universe of potential buyers the same way.

Some founders are reluctant to sell into public-company structures where their businesses become regional reporting units inside much larger organizations. Others may hesitate at becoming part of globally owned enterprises where local autonomy could feel uncertain.

For sellers who care deeply about continuity – for employees, customers, and operating culture – the appeal of a culturally aligned private acquirer can be compelling.

That’s where Eastwood appears to be positioning itself – not merely as a buyer, but as a preferred, durable steward of the trustmark that the Peachtree Building Group sustained over the decades.

The private buyer advantage has come of age

Public homebuilders still retain undeniable acquisition advantages. They can access capital markets more efficiently. Public equity can function as acquisition currency. Their purchasing power is formidable. Their operating infrastructure is already scaled.

But increasingly, private multi-regional builders are proving they bring different strengths to competitive acquisition conversations.

They can often move faster. Their decision-making structures tend to be less bureaucratic. They are not under constant quarterly earnings scrutiny. Their strategic time horizon may be longer and less reactive. And perhaps most importantly, in founder-to-founder transactions, they may offer greater cultural familiarity.

JTW Advisors’ latest market analysis points directly to this shift, highlighting “foreign and privates with long-term strategies” as particularly active buyer groups in the current environment.

That characterization captures something essential about the present M&A cycle. These are not distressed opportunists shopping for discounted assets. They are strategic platform launch pads.

The private acquirer cohort increasingly recognizes that scale in homebuilding is no longer simply about bragging rights or market-share optics. It is about operating economics, resilience, and competitive durability in a structurally more demanding environment.

Eastwood is increasingly behaving like a company with exactly that mindset.

Mapping opportunity

Another notable shift in homebuilding consolidation is geographic.

Historically, homebuilder M&A activity concentrated overwhelmingly in major primary markets. JTW’s data shows that the pattern is changing meaningfully, with secondary-market transactions now representing a majority of recent activity.

That evolution reflects a broader reality about where sophisticated operators believe opportunity exists.

Some of the strongest private builders have built their businesses not by chasing only the largest headline metros, but by winning in markets where operational discipline, local relationships, and disciplined execution create durable competitive advantages.

Atlanta, of course, does not fit neatly into the secondary-market category.

But Eastwood’s broader expansion strategy appears philosophically aligned with the same logic: build a resilient regional operating footprint rather than simply accumulating marquee market names. Regional density often creates advantages that disconnected geographic expansion cannot.

Shared leadership capabilities, overlapping trade relationships, market intelligence transfer and operating consistency become easier when a company grows within coherent regional corridors.

Eastwood’s Southeastern push increasingly resembles that model.

Competitive smoke signal

The temptation will be to view the Peachtree acquisition as an incremental tuck-in. Big mistake. Eastwood now operates with meaningful multi-market scale, and scale changes the competitive equation.

A builder with broader geographic reach can spread overhead more efficiently. It can recruit leadership talent and offer broader career pathways. It can justify greater investment in systems, technology, and process improvement. It can redeploy capital across markets based on relative opportunity rather than local necessity.

It also gains something especially valuable in uncertain housing cycles: optionality.

If demand slows in one market, stronger performance elsewhere can offset pressure. If land becomes constrained or overpriced in one geography, investment can shift. If product demand changes by price segment or consumer profile, operating diversity creates flexibility.

Scale does not eliminate execution risk, but the Eastwood operational system is proving to be a resilient, high-performing real-life value stream. This improves the Eastwood team’s strategic maneuverability.

The larger story is what the transaction says about where homebuilding consolidation is headed.

Public builders remain powerful acquirers. Japan’s global housing giants continue making bold U.S. moves. Institutional capital remains active.

But another force is increasingly shaping the market.

The rise of the strategically ambitious multi-regional private acquirer.

------------Read More

By: John McManus

Title: Eastwood Homes lands Peachtree Building Group in Atlanta

Sourced From: www.housingwire.com/articles/eastwood-peachtree-acquisition-atlanta/

Published Date: Tue, 26 May 2026 21:41:34 +0000